ResearchersChristian Irlbeck, Grier Tumas Dienstag, Leda Zaharieva, and Matthew Scally, with Richard Zhang and Ritapa Ray, representing views from McKinsey’s Insurance Practice, published an article in February 2026 regarding how AI is affecting insurance. The article provides an p-to-date review of this issue. Here are some key issues.

The insurance industry represents a significant opportunity for AI to drive value creation, and the technology will continue making inroads across the industry in the months and years ahead.

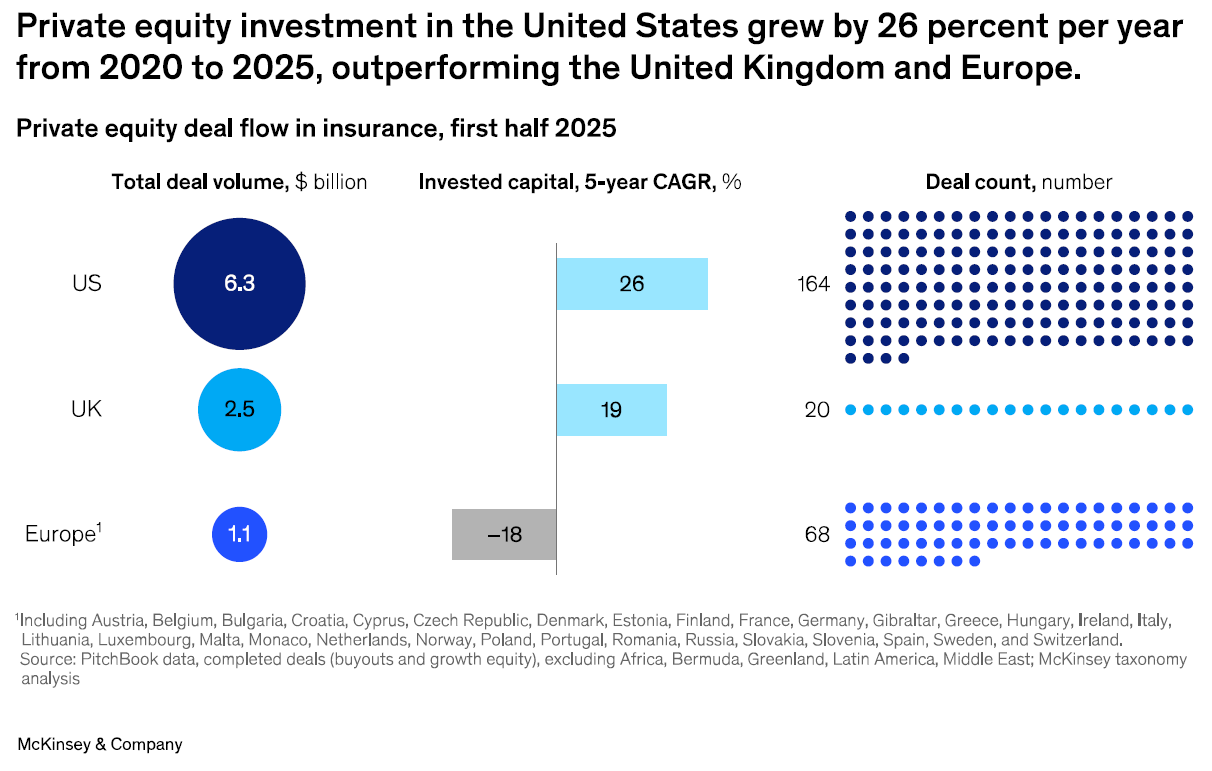

The potential for AI-driven portfolio value creation

The insurance industry sits on immense pools of structured and unstructured data, and many workflows across the value chain are still handled manually. At the same time, the industry has mounting exposure to complex risks, such as cyberattacks, climate-related and other catastrophes, and even AI itself. These dynamics create prime conditions for technology adoption, and the researchers see the sector progressing along an “AI staircase”:

- Traditional AI in the form of predictive data analytics is already established in fraud detection, pricing, and risk modeling.

- Generative AI is beginning to reshape document-heavy tasks like policy issuance, submissions, and some aspects of claims handling and adjusting.

- An emerging frontier of agentic AI promises to autonomously manage end-to-end workflows, from purchasing to select risk assessment.

While AI will transform parts of the insurance value chain, the authors expect it is more likely to reshape existing models than to disintermediate them. The goal is to methodically identify which assets are meaningfully advancing up the AI staircase and where the technology will most enhance performance and competitiveness.

According to the research, McKinsey estimates that gen AI could unlock $50 billion to $70 billion of insurance industry revenue, with the highest impact on marketing and sales, customer operations, and software engineering dimensions.

The subsectors where AI is reshaping performance.

While many use cases will still require human oversight, AI is already reshaping performance across brokers, managing general agents, software providers, and third-party administrators. These are the individual subsectors and how AI is affecting the investment appetite.

Brokers (retail and wholesale)

As the market matures, value creation is focused not only on roll-ups of brokers (a major theme of the recent past) but also on vertical integration, tech-enabled placement, and data for more consultative risk guidance. AI is an important enabler of this next phase. Rather than replacing brokers and producers outright, it is likely to help them better counsel clients on their risk and expand their margins.

The authors point out that early gen AI use cases are already improving efficiency and conversion. These cases include using AI for automated submission ingestion, carrier appetite matching, and use of placement copilots for renewals and cross-selling. Over time, agentic AI may begin to handle end-to-end renewal for simple risks, dynamically connecting clients and capacity providers with limited human intervention (which brokers would own).

Clients continue to value brokers for tailored and trustworthy advice and access to markets. In fact, rather than replacing the role of the broker, technology is supporting it by enabling novel applications of sales lead generation, and augmented broker tooling.

The investigation indicates that in the longer term the differentiation gap will widen between brokers that use AI skillfully and those that do not.

Managing general agents (MGAs)

MGAs have been one of the fastest-growing subsectors in insurance. MGAs have become central to innovation in insurance, creating demand for more sophisticated use of data and technology. As the market further evolves, AI can create value across both underwriting and distribution. In underwriting, AI is being applied to accelerate and personalize intake and submission, perform highly granular segmentation and risk scoring, and draft tailored documents and messages to streamline communications and facilitate follow-ups as part of issuance and delivery.

In addition to effective AI adoption, owning and activating data will become a defining source of value. MGAs that can consolidate, enrich, and protect proprietary data will become indispensable partners to both brokers and carriers, as they will be able to feed better risk insights back into the ecosystem. The MGAs that combine strong relationships with data ownership and advanced AI use will differentiate themselves most sharply. They will use AI to strengthen, not replace, human underwriting judgment.

Software providers

Software and data platforms remain a fast-growing area of insurance investment, rising by about 20 percent annually on average over the five years through the first half of 2025.

As AI moves from experimentation to adoption, the next frontier for software providers is being shaped not by model performance alone but also by how enterprise buyers are rethinking their architecture and procurement patterns. The researchers stress that their recent cases show that insurers are moving away from monolithic systems and toward modular, open environments that are low best-of-breed AI tools to interoperate—what we have called the agentic AI mesh.

The authors emphasize that as insurers move toward modular architectures and multi-agent collaboration, platforms that enable this agility will command premium valuations and become the backbone of the industry’s next digital chapter.

Third-party administrators

Third-party administrators (TPAs) remain a private equity focal point; average annual growth in deals in this space has increased by about 15 percent in the past five years, according to PitchBook.

It is not yet clear how TPAs will reliably monetize AI-driven efficiency gains. Many TPA commercial arrangements still skew toward head count, activity-based constructs, or cost-plus economics (explicitly or implicitly). Under those models, automation can actually pressure top-line revenue even when performance improves, and higher accuracy or better outcomes are not always directly compensated. This creates a real strategic tension: AI can make TPAs better operators while simultaneously undermining the mechanics of how they get paid.

As a result, the authors expect the next phase of the subsector to be defined less by whether TPAs adopt AI (they will) and more by how they evolve their pricing models and competitive positioning. And as automation reduces the complexity advantage that TPAs have historically held, maintaining cost competitiveness and continuous innovation will remain critical.

Projecting how AI will change talent models.

McKinsey estimates that today’s technologies could theoretically automate more than half of current US work hours. Two-thirds of US work hours today are devoted to nonphysical work—much like that found across the insurance value chain. Current workforces will require evolution and AI upskilling to keep pace. They not only must learn how to integrate with AI processes but also must move from basic tasks to broader framing, interpretation, and actioning of insights.

As the insurance landscape evolves, AI will redefine value creation across every segment of the market.

Four priorities for investors

Most private insurance investors now recognize AI’s disruptive potential, but many are still determining how to act. Some are embedding AI into diligence; others are mobilizing portfolio companies to preserve market position while looking to create new value opportunities. The challenge lies in deciding where to invest based on how AI shifts value, how fast to move, and how to build lasting advantage. In general, four priorities stand out for investors in insurance seeking to turn AI into an eventual portfolio differentiator.