Researchers Andreas Cornet, Ruth Heuss,Andreas, Tschisner, Russell Hensley, Patrick Hertzke, Timo Möller, Patrick Schaufuss, Julian Conzade, Stephanie Schenk and Karsten von Laufenberg from the McKinsey Center for Future Mobility, published an article named: “Why the automotive future is electric”. The article provides an up- to date review on this issue. Here are some of the key issues.

The tipping point in passenger EV adoption occurred in the second half of 2020, when EV sales and penetration accelerated in major markets despite the economic crisis caused by the COVID-19 pandemic. In 2021, the discussions have centered on the end date for internal combustion engine (ICE) vehicle sales. New regulatory targets in the European Union and the United States now aim for an EV share of at least 50 percent by 2030, and several countries have announced accelerated timelines for ICE sales bans in 2030 or 2035. Industry players are accelerating the speed of automotive technology innovation as they develop new concepts of electric, connected, autonomous, and shared mobility. The industry has attracted more than $400 billion in investments over the last decade – with about $100 billion of that coming since the beginning of 2020. All this money stresses the authors, targets companies and startups working on electrifying mobility, connecting vehicles, and autonomous driving technology. Such technology innovations will help reduce EV costs and make electric shared mobility a real alternative to owning a car.

Regulation and technology

Regulatory pressure and the consumer pull toward EVs vary greatly by region. Europe is mainly a regulation-driven market with high subsidies, while in China consumer pull is very strong despite reduced incentives. In the United States, EV sales have grown slowly due to both limited regulatory pressure and consumer interest, although the regulator trend is set to change under the new administration.

On a global level, the researchers expect EV (BEV, PHEV, and FCEV)1 adoption to reach 45 percent under currently expected regulatory targets. However, even this transformative EV growth outlook is far below what’s required to achieve net zero emissions. EVs would need to account for 75 percent of passenger car sales globally by 2030, which significantly outpaces the current course and speed of the industry.

The authors believe Europe– as a regulatory-driven market with positive consumer demand trends – will electrify the fastest and is expected to remain the global leader in electrification in terms of EV market share. In addition to the European Commission target, which requires around 60 percent EV sales by 2030, several countries have already announced an end to ICE sales by 2030. In line with this, seven OEM brands have committed to 100 percent EV sales by 2030 within the European Union. In the most likely accelerated scenario, consumer adoption will exceed regulatory targets and Europe will reach around 75 percent EV market share by 2030. The European Union announced a zero-emissions target for new cars by 2035.

China will also continue to see strong growth in electrification and remain the largest EV market in absolute terms. The study estimates that a Chinese EV share above 70 percent for new car sales in 2030.

In the United States, the Biden administration announced a 50 percent electrification target for 2030, strong investments in charging infrastructure, and more stringent fleet emissions targets.

In the European Union, achieving the accelerated scenario of around 75 percent EV sales by 2030 will have implications for the entire EV value chain and ecosystem. Incumbent automotive suppliers need to shift production from ICE to EV components. Europe will have to build an estimated 24 new battery giga-factories to supply local passenger EV battery demand. With more than 70 million EVs on the road by 2030, the industry will need to install large numbers of public chargers and provide maintenance operations for them. Renewable electricity production needs to increase by 5 percent to meet EV charging demand.

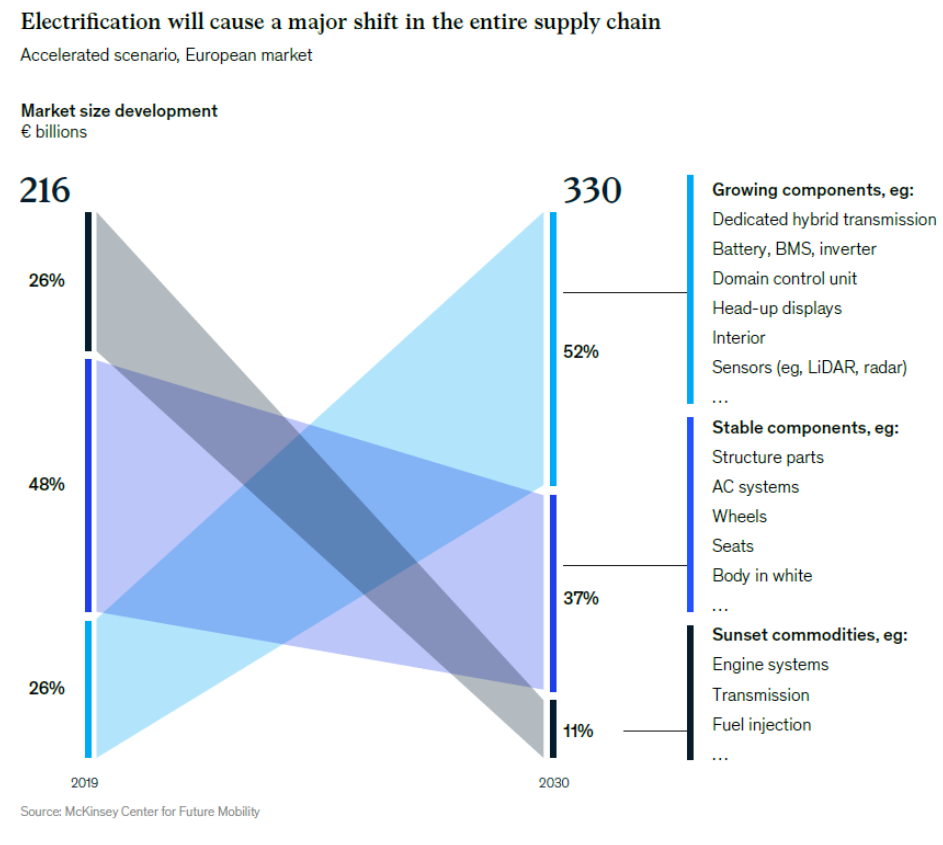

Electrification will cause a major shift in the entire automotive supply chain

According to the study, the transformation of the automotive industry toward electrification will disrupt the entire supply chain and create a significant shift in market size for automotive components. Critical components for electrification such as batteries and electric drives and for autonomous driving like light detection and ranging (LiDAR) sensors and radar sensors will likely make up about 52 percent of the total market size by 2030.

Based on announced buildup plans, the researchers expect a 20-fold increase in battery production capacity in Europe to 965 GWh by 2030. Assuming the full capacity is built by 2030.

Battery cell production is moving physically closer to vehicle assembly plants. While ten years ago almost all cells were imported from Asia, regional production hubs exist today in Eastern Europe, for example. Furthermore, multiple plants will go onstream in key vehicle-producing countries like Germany, the United Kingdom, and France and in low-carbon-emitting environments such as Norway and Sweden.

In line with EV uptake, the buildup of charging infrastructure needs to accelerate to avoid becoming a potential bottleneck and limiting consumer-driven EV adoption. Building charging infrastructure in sync with the EV fleet will be essential in the coming decade. While first-generation EV buyers relied mainly on private charging (in 2020, 80 percent of EV buyers in Europe had access to private charging), the next generation will depend on public charging.

Likewise, regulatory processes to install chargers in private homes require simplification and production capacity for wall boxes must increase. Researchers estimate the industry needs to install more than 15,000 chargers per week by 2030 within the European Union.

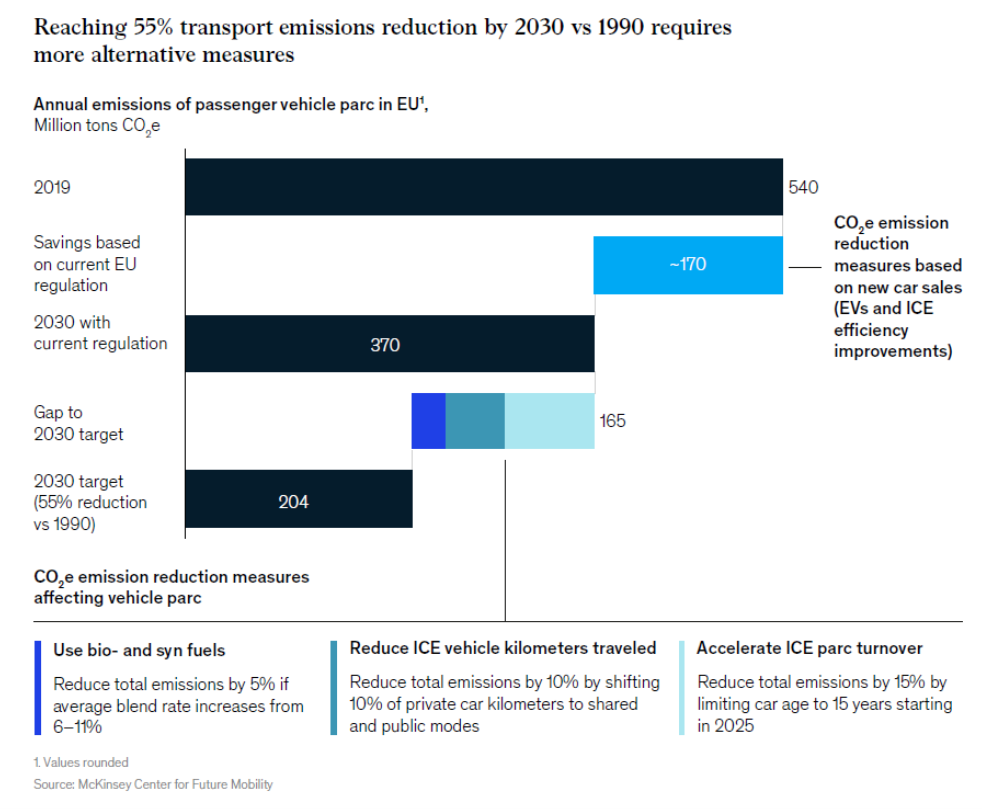

A 55 percent transport emissions reduction target by 2030 versus 1990 requires more drastic measures

The research point out that the current regulation and targets are not sufficient if the road transport sector wants to fully contribute to the 55 percent CO2e emission reduction target by 2030 versus 1990 as required by the Fit for 55 program.

However, passenger cars have one advantage over other industries from a decarbonization point: The zero-emissions option (e.g., the BEV) is cheaper than the current alternative (ICE) from a total cost of ownership perspective in some countries today and by 2025 at the latest in countries without incentives.This is not the case in most other industries, where decarbonizing results in higher costs for both producers and consumers.

However, with the average car age at ten years in Europe, it will take time for EV sales to have an impact at the parc level. The current regulation on sales is therefore not sufficient to meet the goal of a 55 percent emissions reduction from 1990 levels by 2030. Closing this gap, stress the researchers, will require further measures targeting CO2e emissions of the vehicle park. ICE vehicle kilometers traveled could be decreased by reducing private car kilometers, increasing shared mobility, and changing consumer perspectives on walking/biking.

At the same time, the most efficient lever is to accelerate the ICE parc turnover and remove highly polluting ICE vehicles from the fleet with, for example, “cash-for-clunkers” programs for old ICE cars. Another way to reduce CO2e emissions from ICE vehicles is to increase the share of bio- and e-fuels as these have a low carbon footprint and are compatible with the existing ICE parc. However, the majority of bio- and e-fuels supply will be required to decarbonize marine/aviation and commercial road transport, for which only limited zero-emissions alternatives exist today.

Conclusion

Electric vehicles are coming, and we are on the right track regarding decarbonizing the transport sector, though more actions need to be taken. It is an industry transformation taking place at unprecedented speed. It is also crossing industry borders, involving energy, infrastructure, mobility, and automotive players. While a major challenge, it represents a huge opportunity for incumbents and new players to take a leading role in creating new multi-billion industries and jobs. The key, the author emphasizes, will be to couple sustainability with economic viability through innovative technology and properly guided mobility transformation. Based on its diverse mobility landscape, its focus on sustainability and its proven technology leadership, Europe could emerge as a role model for other regions globally.