Researchers Nathan Niese, Aakash Arora, Elizabeth Dreyer, Aykan Gökbulut, and Alex Xie from the Boston Consulting Group published an article on June 09, 2022 regarding electric cars. The article provides an up-to date review on this issue. Here are some of the key issues.

The world stands on the threshold of a new age of electrified mobility thanks to developments over the past year. Spurred by a renewed sense of urgency, regulators in Europe and the US have set far more demanding goals for curbing greenhouse gas emissions from cars and light vehicles. Automakers have also raised their game and introduced electric vehicle (EV) options in every part of their product portfolios. Together, these forces are turbocharging the global market for EVs.

A Bumper Year

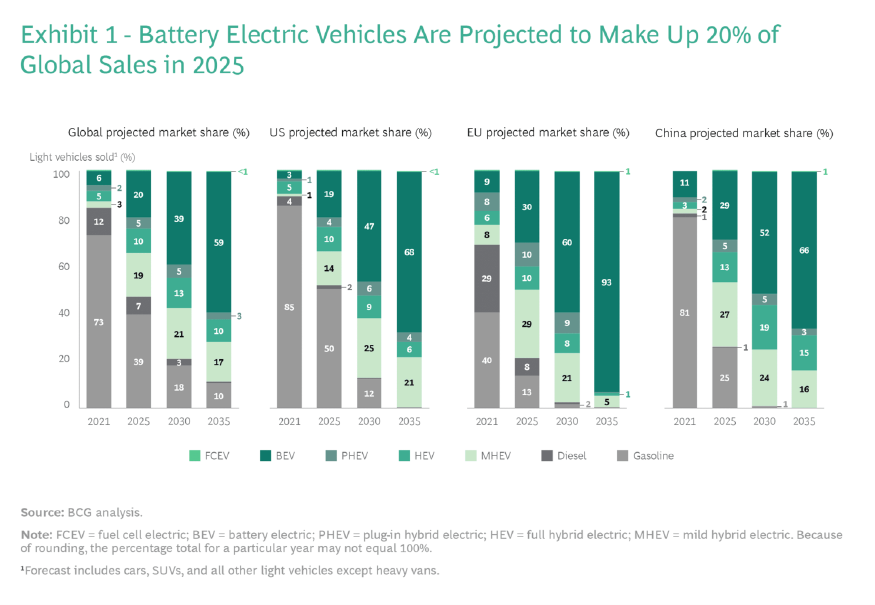

The past year has been phenomenal for electric vehicles, including hybrids. These vehicles accounted for 20% of all light-vehicle production in 2021, up from 12% the previous year, even as volumes recovered from the COVID-19 pandemic. By contrast, the share of gasoline and diesel cars dipped 9 percentage points.

The regulatory pressures curbing the use of fossil-fuel-powered vehicles have increased in major Western markets. In the US, the Biden administration significantly tightened rules on tailpipe emissions. EU legislators drafted policies to reduce the average emissions of all cars in operation by 55% by 2030 (from 2021 levels). More importantly, by stipulating that emissions from new vehicles sold should be decreased to zero five years later, they set an end date for the ICE age in Europe. In both regions, governments have extended incentives encouraging consumers to switch to low-emission vehicles.

Automakers have thrown their support behind EVs like never before. Toyota and Volkswagen, the two largest automakers by sales today, have committed a combined $250 billion by 2030 to EV and battery programs.

Falling ownership costs and incentives have helped drive consumer demand for EVs. The five-year total cost of ownership (TCO) for a midsize car is now the same for both BEV and ICE versions in China and many European countries.

The continuing decline in battery prices, which make up 30% to 40% of an EV’s cost of goods sold, is one factor leading to lower ownership costs. But so too are greater economies of scale due to increased production of EVs.

An Industry in Transition

The future of the automotive industry is electric. Researchers now expect BEVs to account for 20% of global light-vehicle sales in 2025 and 59% in 2035.

At the same time, the authors stress that the shift toward EVs is causing incumbent automakers to reconsider not just the transition from ICE power trains to electric ones but their entire business models. These companies are executing vertical-integration moves that improve access to battery cells, secure first rights to next-generation battery technologies, and drive higher performance of electric motors.

Automakers are also adopting simplified electronics architectures and a more software-driven approach to drive down costs, unlock new revenue streams, and offset lower near-term margins on EV sales. Through over-the-air updates (the wireless delivery of new software and capabilities), for example, manufacturers can remotely extend the range of EV batteries or enable EV owners to automatically pay for charging infrastructure through vehicle recognition technology. All told, savvy automakers—both incumbent and new age—are recognizing that the shift to EVs significantly boosts the size of the profit pools available to the automotive industry.

Improved Progress on Climate Goals

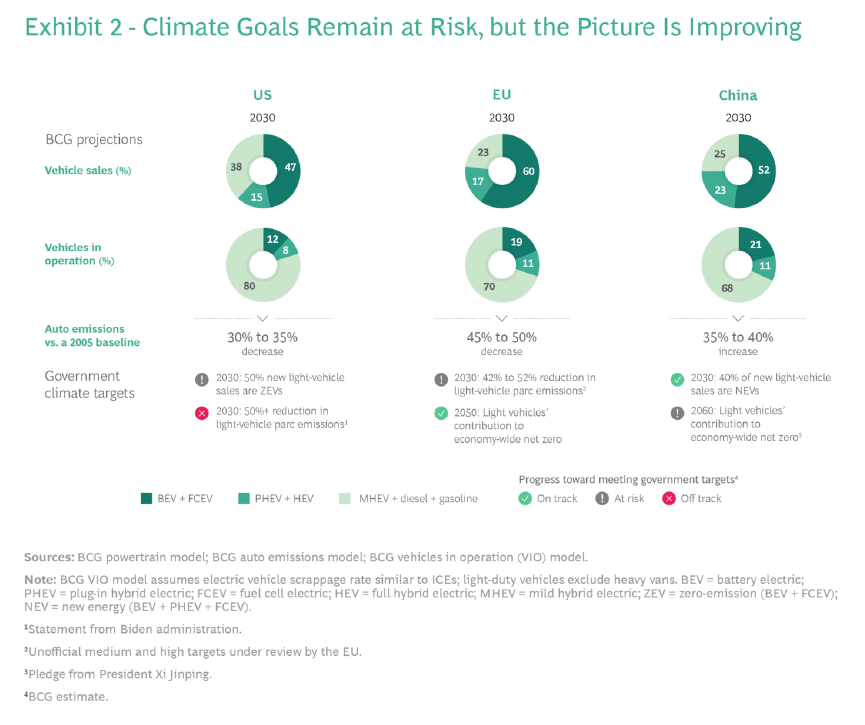

The study point out that by preparing to stop the sale of new fossil-fuel cars from 2035 (the ban should become legally binding next year or in 2024), the European Union is on track to achieve its goal of net-zero CO2 emissions in its “car parc”—the total stock of vehicles in use—by 2050, provided the bloc also continues to invest in mass-transit systems and clean-mobility options such as e-bikes. By then, almost all vehicles on European roads should be zero emission.

Given that EVs accounted for more than 20% of new light-vehicle sales in China earlier this year, we now expect that country to meet its 2030 target for 40% of vehicles sold to be pure electric. All new light-vehicle sales in China will need to be EVs by 2040 for the nation to achieve its 2060 net-zero goal.

The US will need to ban sales of new vehicles other than zero-emission ones by 2035—just as Europe is doing—to fulfill its 2050 net-zero pledge.

It’s not just vehicles that will generate zero emissions because of electrification. The entire automotive value chain is moving toward decarbonization.

Some Remaining Risks to EV Adoption

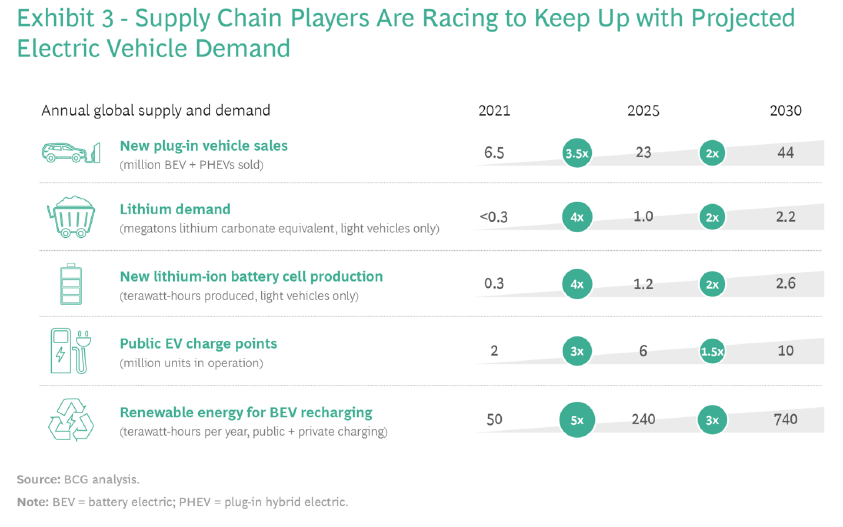

Although the transition to electrified mobility is quickly gathering momentum, the research has identified two short-term supply risks that could limit the rate of industry change—or spur greater innovation as players seek to overcome these obstacles. First, a supply shortage has emerged during the past half year in the metals needed to make EV batteries, including lithium and nickel. Second, insufficient charging infrastructure over the next few years could cause EV adoption to stall in leading markets.

Demand for lithium, for example, is expected to shoot up by a CAGR of more than 25% from now until 2030. But post pandemic supply chain constraints, rising energy costs, and accelerated EV growth have already increased the price of the lithium compounds used for battery production—and are set to push up average battery costs after years of steady declines. Meanwhile, war and economic sanctions have raised nickel prices and threaten to exacerbate shortages of the metal.

A shortage of charging points in some countries looks set to worsen in the near future. In the UK, the automotive industry organization recently highlighted that current EV sales far outpace the growth in public charging stations.

Concern about a lack of public charging sites is already the leading reason for US consumers to think twice about buying an EV, according to a recent survey from Consumer Reports, a nonprofit consumer organization.

A New Game

Coordinated action will be essential to overcome the challenges we have outlined. Fortunately, there is reason for optimism that players across the automotive ecosystem are prepared to work together, instead of treating the development of viable solutions as a zero-sum game of winners and losers.

In the charging space, a raft of players are helping to accelerate the rollout of publicly available chargers. Governments are freeing up land and supporting ambitious projects such as wireless EV charging. Manufacturers are creating prefabricated charging sites to shorten installation times.

Through innovation, automakers are also taking EV battery recharging to the next level. They are developing new battery-swapping and battery-as-a service models, options that are already popular among drivers of electric two- and three-wheel vehicles. For example, China’s Nio offers customers a subscription-based service enabling them to exchange used batteries for new ones at one of its battery swap stations.

To improve supply chain resilience, automotive manufacturers and battery makers as well as cathode suppliers are forming joint ventures and investing in mines.

The authors conclude that what these actions show is that—when confronted with significant challenges— the automotive industry is quick to innovate. The proof: leading automakers today are still delighting customers and creating value for shareholders. But they are also setting an example for other sectors on how to respond to the climate change challenge.