In the article “Exemplary cases for the development of the “Italian way to connected mobility”: cities and the creation of urban connected ecosystems” some of the examples of smart development of cities, both in Europe and overseas (USA), in which Connected Mobility plays a key role, were examined in depth. These are tangible examples that demonstrate how the combined use of connectivity and mobility data can enable the realisation of Vision Zero: Zero Accidents, Zero Congestion, Zero Pollution.

As far as European cities are concerned, the two emblematic cases are represented by the city of Frankfurt (in partnership with the city of Dortmund) and the city of Hamburg. Both case studies are located in Germany and this should not come as a surprise: Germany has in fact been engaged for years in the development of new mobility management models in cities through data, also through the involvement of an increasing number of private actors. It should be noted that, in the German vision, the role of the public sector in launching these initiatives is also intended to act as a stimulus for innovation in the automotive sector’s value chains. Overseas, the case of the city of San José, in the heart of California’s Silicon Valley, was analysed. According to the vision of the municipality of San José, a ‘smart city’ must be able to create an experimental environment in which new technologies and data-driven decision-making processes drive continuous improvement in the services offered to citizens.

In this article, some data on new mobility models are reported and some examples of studies, identified in the global context, are provided, with the aim of defining the lines of development and the potential that could be generated by the diffusion of new mobility models. In particular, the diffusion of self-driving vehicles and sharing services has been studied. In both cases, in order to encourage their increasing diffusion, it will be necessary to rethink the way in which mobility is conceived and to create adequate infrastructures.

As mentioned, thetwo models chosen are closely interrelated, with autonomous driving being positioned as the technology that will enable the full potential and benefits of sharing mobility models, as discussed below.

Self-driving vehicles are classified based on five levels of capability: the first level (L1) corresponds to driving support systems, while the last level (L5) corresponds to a fully autonomous vehicle capable of moving without user support[1].

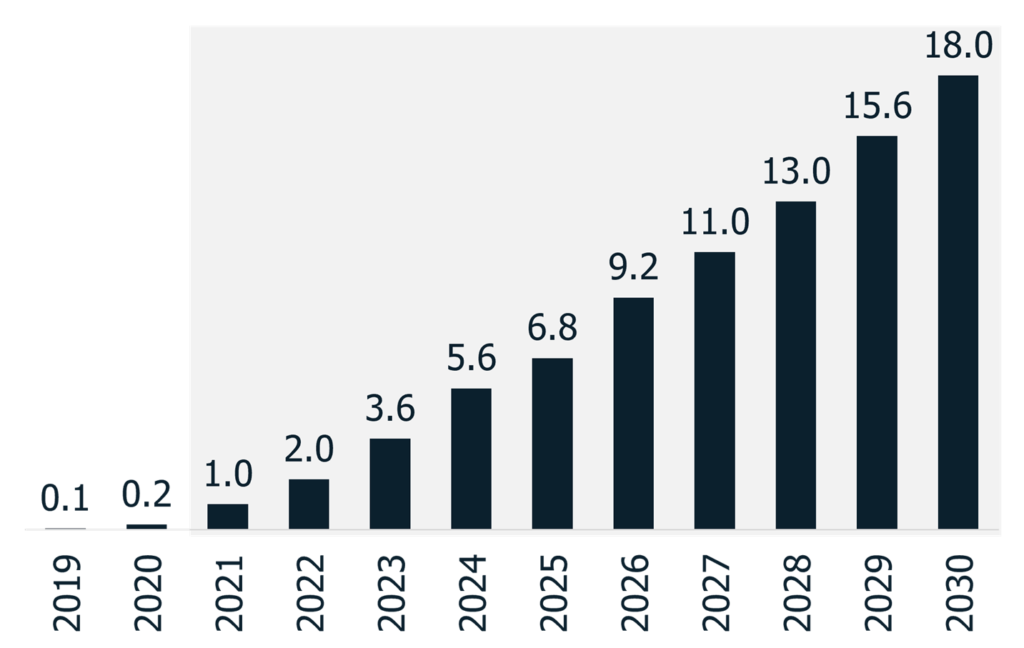

To date, most autonomous driving systems belong to the first classes (L1 and L2) and are mainly used to provide driving assistance. In the next few years, this trend will change: it is estimated that by 2030 the number of self-driving cars of Level 3 (so-called ‘conditional autonomous‘, i.e. a vehicle that can read and interpret road signs but still requires some driver support) or higher will increase by 90 times compared to 2020[2].

From 2025, more than 30% of cars sold will be equipped with at least Level 4[3].

The self-driving vehicle will make it possible to break free from the need for ownership and will transform the current model of use: the use of a self-driving vehicle in a ride-hailing logic could generate savings of more than EUR 5,000 per year compared to the use of a proprietary vehicle[4].

In relation to this first area, we chose to analyse ‘Endeavour’, a project built on mechanisms of partnership and collaboration with different types of actors, from local authorities, road safety groups, universities, transport providers and, above all, the general public[5]. The Endeavour project is the first trial of the services, capabilities and potential of autonomous vehicles, carried out in multiple cities across the UK. Now in the final stages of testing, the project will culminate with a final demonstration at an event in Greenwich in August 2021.

The testing of the Endeavour project was carried out using four Ford Mondeo vehicles equipped with LiDAR, RADAR and cameras. All these systems were integrated with the autonomous driving software platform of Oxbotica – a spin-off company of Oxford University. The fleet, capable of achieving a level 4 autonomy (out of 5 levels, so these vehicles are almost completely capable of moving without driver support), carried out the latest tests in a five-mile area around Lea Hall station, between Birmingham International Airport and the city centre.

The trials were conducted continuously – day and night – for several weeks, allowing Oxbotica’s autonomous vehicles to experience different traffic scenarios and weather conditions. The routes included different scenarios and combinations of scenarios, including roundabouts, traffic lights and intersections in both industrial and residential areas – all of which were used to put the autonomous vehicles through their paces, test their self-driving capabilities and collect data to improve the vehicles’ automation software[6].

In the global context, there is also a new mobility model – represented by sharing mobility – which brings with it a paradigm shift: from ownership to possession and sharing of a means of transport.

Sharing is a model through which to pursue in a synergic way the needs of cities, e.g. in terms of decongestion, and, at the same time, the needs of citizens who aim to have access to flexible forms of transport (i.e. on-demand services) without the burdens and critical points of an owned car (e.g. insurance, revision, maintenance, etc.).

Moreover, sharing services are considered promising solutions for a sustainable transport future, given the reduction in average vehicle ownership, emissions and kilometers travelled[7].

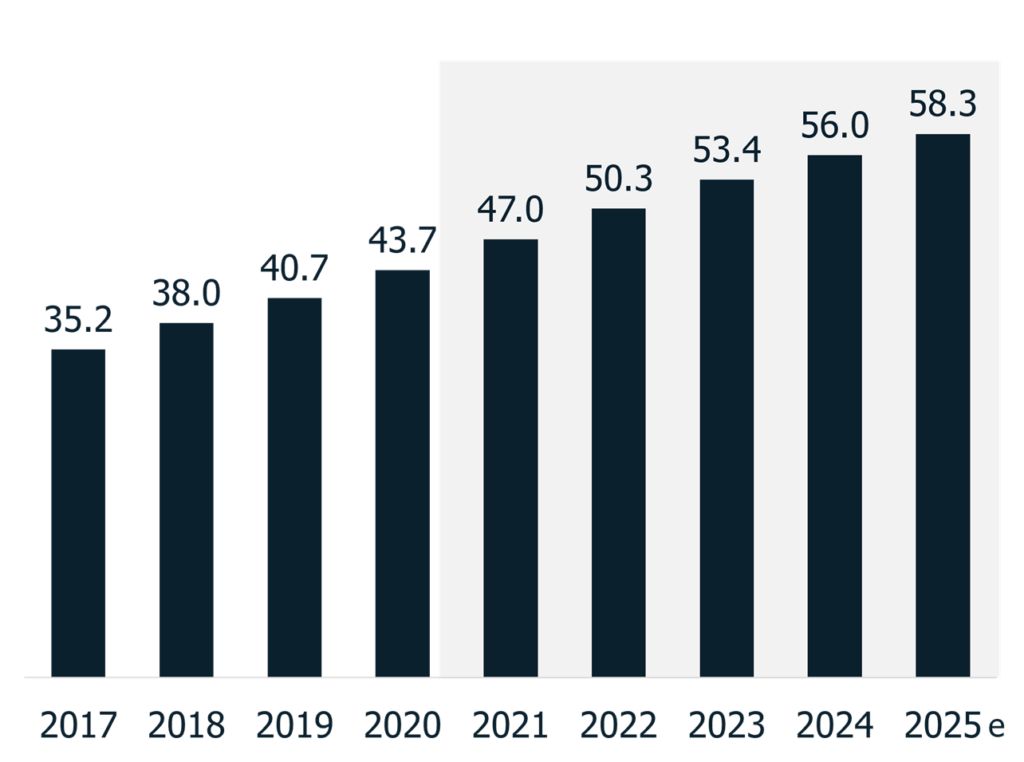

The carsharing phenomenon is booming worldwide: carsharing users increased by +24.1% from 2017 to 2020 and a further +33.4% increase in carsharing users is expected over the next 5 years (2025 vs. 2020)[8].

The phenomenon is also present in our country: to date in Italy there are more than 2.5 million people registered on the various platforms and 10 million rentals. Italy is the second country in Europe for car sharing services, after Germany:

- In 2020, the market consisted of 15,000 vehicles with a turnover of €357 million.

- In 2025 a market of 44,000 vehicles and 725 million euros is expected[9].

According to a study conducted in Germany, the availability of shared mobility services is inducing a change in mobility preferences, mainly characterised by an increase in cycling and walking as well as carpooling. At the same time, the spread of car sharing allows a more efficient use of resources through a higher degree of vehicle utilisation with a potentially larger pool of users[10].

Multimodal mobility, defined as the use of a network composed of different transport modes for mobility needs, seems to be a promising route to further enhance the positive environmental benefits of classical (ergo single mode) sharing systems. For example, the integration of bicycles and public transport by offering an all-inclusive service via a single app[11].

As a practical example of the sharing model, we chose to analyse what has been developed in the Czech Republic. Students from three universities – the University of Economics in Prague, the Technical University in Prague and the University of Life Sciences in Prague – developed a unique car sharing concept called “Uniqway”. One of the main objectives of the project is to create a community of users interested in the sharing economy and to facilitate access to affordable and efficient (including emissions) transport for the Prague university community.

Since 2018, the platform’s services have been available to students and employees of the three universities. Uniqway became real thanks to a collaboration agreement between the universities and several private players, including SKODA AUTO and SKODA AUTO DigiLab, who provided concrete support by providing the first vehicles and a mentorship service.

The three universities then shared the various management roles of the platform: students from the Prague University of Economics are responsible for the project’s marketing strategy and social networking, while students from the Czech Technical University developed the technical concept and design of the service and students from the Czech University of Life Sciences Prague oversee project administration.

The ‘Uniqway’ platform is constantly being improved, for example, the Reward Shop has recently been introduced, giving users the opportunity to buy Uniqway products and merchandise. Another recently introduced service relates to vehicle sanitation and management: the fleet of vehicles is carefully looked after by a team of specialists, ensuring that the cars are clean, disinfected and always present where they are most needed.

According to some studies, the two models – self-driving vehicles and sharing – can be combined to generate important savings:

- Reduce the total cost per km travelled by -46.5%.

- Reduce the total annual running cost of a vehicle by -46.3%.

- Reduce harmful gas emissions by -80% by 2050.

- Optimising integration between LPT and sharing mobility[12].

In the vision of OCTO and The European House – Ambrosetti, to achieve these results it will be essential to rethink the entire mobility ecosystem.

According to the evidence that emerged during the research, the The European House – Ambrosetti and OCTO Working Group has defined a series of elements to work on in order to develop a vision of the customer centric mobility ecosystem: as has already happened in other industries, for example the financial sector, business models will have to increasingly keep customers in mind and focus the value proposition on the creation of a complete and satisfying consumer experience.

Adopting a customer-centric point of view, The European House – Ambrosetti has identified three macro-blocks at the basis of the future mobility ecosystem:

- Availability of mobility assets – access to different types of vehicles and vehicles, management of vehicle maintenance, availability of space, ease of refuelling and recharging.

- Buying experience and marketplace – simplicity of customer interface, aggregation, offer and sale of mobility services per user, offer and sale of smart services.

- Smart service factory – availability of smart services for drivers, cities and fleet managers.

Each macro-block consists of a series of added value services that could enrich the mobility and travel experience. Just to mention a few examples: the possibility of choosing different forms of mobility based on needs, even in aggregate form; platforms as enablers of new forms of supply and services in an integrated way; improving city mobility management, flows and spaces, LPT flexibility, air quality and road maintenance through the use of data.

At the intersection of the three macro-blocks, a new model of mobility is identified, defined as Mobility-as-a-Service – i.e. mobility whose services are all within the reach of smartphones -, based on the optimisation of the user experience, enriched by the interaction between the different components of the ecosystem, and on alignment with Vision Zero (Zero Accidents, Zero Congestion, Zero Pollution) – described in the previous article in this series.

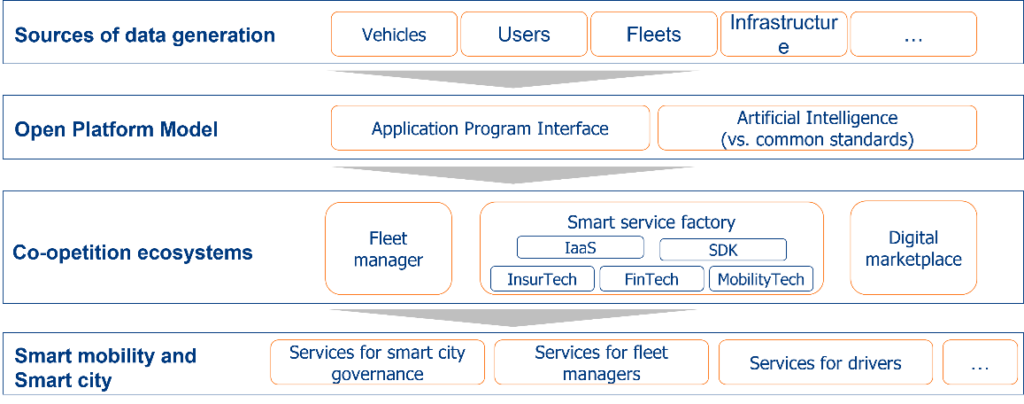

To enable this new mobility model, two key elements need to be promoted and stimulated within the various mobility stakeholders: firstly, the importance of data and the need for openness, and secondly, the adoption of the platform model and the opportunity for co-opetition.

When combined, asset availability, marketplace and smart service factory create a new customer centric mobility ecosystem capable of generating more value than optimising individual businesses.

In concrete terms, with regard to the mobility ecosystem, we believe it is plausible to create an open interoperable model in which the players, belonging to different components of the value chain, adopt collaborative logics from which to benefit by combining their respective competitive advantages to generate new offers and new experiential models for customers.

Ultimately, it can be said that the possibility of creating a connected ecosystem, in which the different mobility actors contribute with different data sources, will enable the creation of new content to serve the different users of mobility services. In the new connected ecosystem, vehicles, users and environments will be able to communicate and exchange information, giving rise to new possibilities for value creation and optimisation of the mobility ecosystem as a whole.

The next article in this series will introduce the pilot projects, outlined by OCTO and The European House – Ambrosetti thanks to the insights and data collected during the initiative. Recalling that the launch of the pilot projects will take place in September, on the occasion of the Final Forum for the presentation of the work (scheduled for 17 September in Rome), the next article aims to serve as an introduction to outline the key points, the operating scheme and the vision proposed by OCTO and The European House – Ambrosetti.

[1] Source: elaboration by The European House – Ambrosetti on European Transport Research Review, 2021.

[2] Source: The European House – Ambrosetti elaboration on market data, 2021.

[3] Ibid.

[4] Source: elaboration by The European House – Ambrosetti on market data, European Transport Research Review, Stanford University and Reuters, 2021.

[5] Source: elaboration by The European House – Ambrosetti on Oxbotica UK website, 2021.

[6] Ibid

[7] Source: elaboration by The European House – Ambrosetti on the paper “Understanding user attitudes and economic aspects in a corporate multimodal mobility system: results from a field study in Germany”, European Transport Research Review (2020), 2021.

[8] Source: The European House – Ambrosetti elaboration on data from the National Observatory of Sharing Moblity, 2021.

[9] Source: The European House – Ambrosetti elaboration on Open Mobility Foundation, IMF and World Bank, 2021.

[10] Source: elaboration by The European House – Ambrosetti on the paper “Understanding user attitudes and economic aspects in a corporate multimodal mobility system: results from a field study in Germany”, European Transport Research Review (2020), 2021.

[11] Ibid.

[12] Source: elaboration by The European House – Ambrosetti on paper “Models, Algorithms, and Evaluation for Autonomous Mobility-On-Demand Systems” by Pavone et al; paper “Autonomous Mobility-on-Demand Systems for Future Urban Mobility” by Pavone, 2021.

Authors:

Alessandro Viviani : Senior Consultant – Innotech Hub

Corrado Panzeri : Associate Partner – Head of InnoTech Hub

The European House – Ambrosetti