Researchers Marcelo Azevedo, Magdalena Baczyńska, Ken Hoffman, and Aleksandra Krauze – Mc Kinsey’s Researchers – provide an interesting up-to-date review regarding the new production technologies for lithium mining and their impact in the production of Electric Vehicles. Here there are some of the key issues.

Lithium is needed to produce virtually all traction batteries currently used in EVs as well as consumer electronics. Lithium-ion (Li-ion) batteries are widely used in many other applications as well, from energy storage to air mobility. As battery content varies based on its active materials mix, and with new battery technologies entering the market, there are many uncertainties around how the battery market will affect future lithium demand.

However, despite expectations that lithium demand will rise from approximately 500,000 metric tons of lithium carbonate equivalent (LCE) in 2021 to some three million to four million metric tons in 2030, the authors believe that the lithium industry will be able to provide enough product to supply the burgeoning lithium-ion battery industry.

Alongside increasing the conventional lithium supply, which is expected to expand by over 300 percent between 2021 and 2030, direct lithium extraction (DLE) and direct lithium to product (DLP) can be the driving forces behind the industry’s ability to respond more swiftly to soaring demand.

However, the study points out that satisfying the demand for lithium will not be a trivial problem. In fact, despite COVID-19’s impact on the automotive sector, electric vehicle (EV) sales grew by around 50 percent in 2020 and doubled to approximately seven million units in 2021. At the same time, surging EV demand has seen lithium prices skyrocket by around 550 percent in a year: by the beginning of March 2022, the lithium carbonate price had passed $75,000 per metric ton and lithium hydroxide prices had exceeded $65,000 per metric ton (compared with a five-year average of around $14,500 per metric ton).

Lithium demand factors

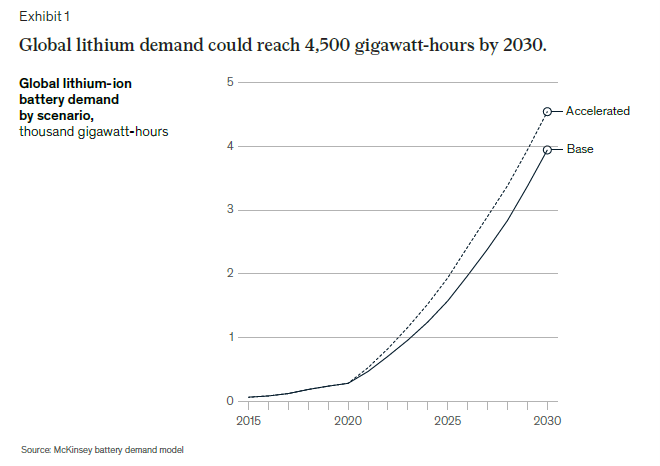

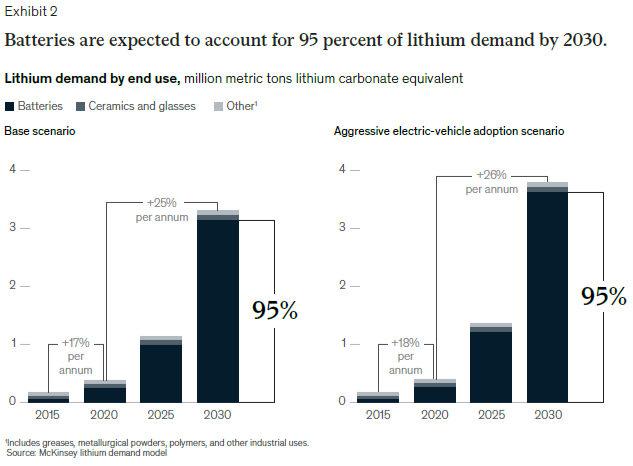

Over the next decade, McKinsey forecasts continued growth of Li-ion batteries at an annual compound rate of approximately 30 percent. Not long ago, in 2015, less than 30 percent of lithium demand was for batteries; the bulk of demand was split between ceramics and glasses (35 percent) and greases, metallurgical powders, polymers, and other industrial uses (35-plus percent). By 2030, batteries are expected to account for 95 percent of lithium demand.

With this soaring demand, should the world be concerned about future lithium supply? In 2020, slightly above 0.41 million metric tons of LCE were produced; in 2021, production exceeded 0.54 million metric tons (a 32 percent year-on-year increase). Mc Kinsey current base-case analysis sees lithium demand of 3.3 million metric tons or a compounded 25 percent growth rate. Due to the short lead times associated with new lithium production, researchers only have visibility of 2.7 million metric tons of lithium supply in 2030; the researchers expect the remainder of the demand to be filled by newly announced greenfield and brownfield expansions.

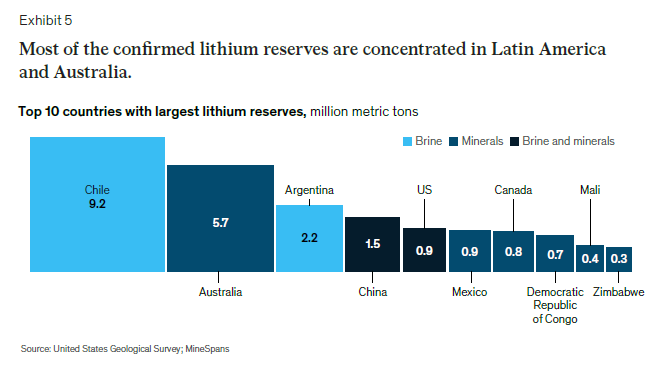

Currently, almost all lithium mining occurs in Australia, Latin America, and China (accounting for a combined 98 percent of production in 2020). An announced pipeline of projects will likely introduce new players and geographies to the lithium-mining map, including Western and Eastern Europe, Russia, and other members of the Commonwealth of Independent States (CIS). This reported capacity base should be enough for supply to grow at a 20 percent annual rate to reach over 2.7 million metric tons of LCE by 2030.

While forecasted demand and supply indicates a balanced industry for the short term, there is a potential need to galvanize new capacity by 2030. Additional lithium sources required to bridge the supply gap are predicted to come from early-stage conventional mineral and brines projects, as yet unknown resources, and unconventional brines such asgeothermal or oilfield brines. Meanwhile, the study emphasizes that new technologies such as DLE and DLPare expected to boost recovery and capacity. In addition, the use of direct shipping ore(DSO) could help mitigate short-term undersupply risk, as it did in 2018.

Unconventional brines (geothermal, oilfield brines)

Additional potential comes from unconventional deposits of geothermal and oilfield brines with grades of 100 to 200 ppm. The first option focuses on providing both clean geothermal energy and lithium supply. Although nothing has been proven on a commercial scale as yet, there are already financially confirmed projects in Europe and North America with some early-stage assets in the pipeline. The authors anticipate that, with technology development and proof of concepts, more geothermal lithium brine operations will appear on the global map, with some OEM and automotive companies already supporting even less advanced assets.

Additionally, projects in North America are focused on extracting lithium from oil-field wastewaters. Although usually low-grade, this can be an additional resource base if the right technology is forthcoming.

Direct lithium extraction

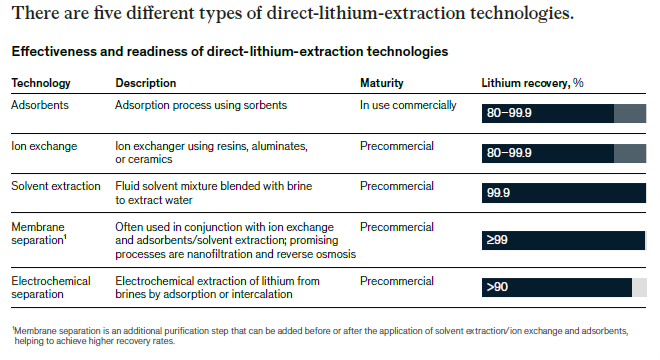

For geothermal or oilfield brines to succeed as a source of lithium supply, a proven process for DLE will be required. There are a number of companies testing various DLE approaches. While their ideas differ, the concept remains the same: letting the brine flow through a lithium-bonding material using adsorption, ion-exchange, membrane-separation, or solvent-extraction processes, followed by a polishing solution to obtain lithium carbonate or lithium hydroxide.

Promising DLE technology is currently being considered not only by unconventional players but also by companies that traditionally develop “typical” brine assets. DLE has several potential benefits, including:

— eliminating/reducing the footprint of evaporation ponds

— decreasing production times compared with conventional brine operation

— increasing recoveries from around 40 percent to over 80 percent

— lower usage of fresh water, which can be one of the deciding factors when applying for a mining concession in a region with scarce water resources

— lower reagents usage and increased product purity (in terms of magnesium, calcium, and boron) compared with conventional brine operations

To date only adsorption DLE has been used on a commercial scale, in Argentina and China. If DLE can be scaled up and spread across brine assets, it will boost existing capacities via increased recoveries and lower operating costs, while also improving the sustainability aspects of operations.

Direct lithium to product

Similar to DLE, DLP technology looks to contain only the lithium metal in a polymer, and then for the lithium to be removed to an electrolyze tube and made into a final lithium product. If successful, this potential process for lithium production could have a significant impact on supply.

Direct shipping ore

The researchers indicate that another option for covering the risk of short-term undersupply, should new capacity deployment be delayed, is supplying DSO to the market. This low-grade spodumene concentrate can be brought to the market with a very short lead time (less than a year for a brownfield project), with resulting sales contributing toward the construction of a full-scale spodumene processing plant.

Refining DSO is more costly and challenging, but 2018 provided an example of how it can be done. Amid a landscape of high prices and an undersupplied market environment, Chinese refineries imported spodumene concentrates from Australia below 1.5 percent lithium oxide (0.7 percent lithium) in order to supply market needs.

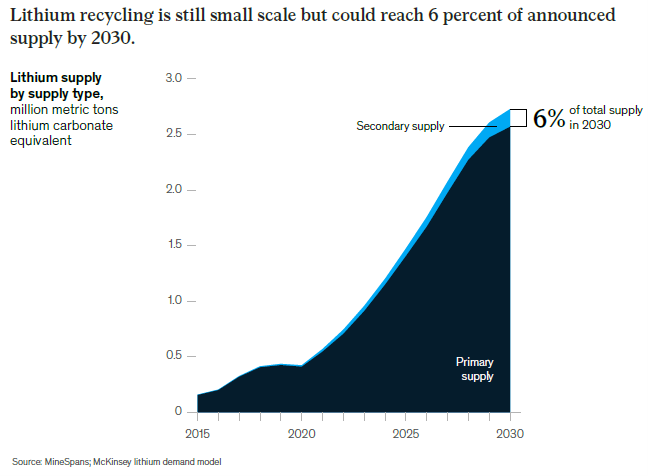

Reuse and recycle

A frequently asked question is whether L-ion batteries can be recycled. With expected battery lifetimes of around ten to 15 years for passenger vehicles, and the possibility of extending EV battery life through use in the energy-storage sector, battery recycling is expected to increase during the current decade, but not to game-changing levels. Depending on the recycling process employed, it is possible to recover between zero and 80 percent of the lithium contained in end-of-life batteries. By 2030, such secondary supply is expected to account for slightly more than 6 percent of total lithium production.

What comes next?

So, will the world secure enough lithium for the upcoming EV revolution? The authors believe it will, but specific actions need to be taken at each level of the lithium value chain:

— Funding new technologies. For example, DLE can boost lithium production from conventional brines by increasing levels of recovery. It can also enable lithium production from assets where lithium is currently “locked,” such as geothermal or oilfield brines.

— Exploration for new projects. In 2021, almost 90 percent of lithium mining took place in just three countries (Australia, Chile, China). Expanding into other regions for new sources of lithium can contribute to developing a new resource base for mining.

— Early warning of manufacturers’ requirements.

Depending on how battery technologies develop, the industry will need more lithium carbonate or lithium hydroxide. Accordingly, end users such as OEMs and those involved in computer-aided manufacturing can help by signaling product specifications and required volumes of lithium early on. Announcing such needs well in advance will give lithium miners enough time to adapt.