Researchers Tanguy Catlin, senior partner in McKinsey’s Boston office, Ani Kelkar and Doug McElhaney, partners in McKinsey and Dimitris Paterakis, consultant in Mc Kinsey’s New York office published an article on Mc Kinsey Global Publishing in April 2024, regarding the auto insurance in the new mobility era. The article provides an up-to-date review of this issue. Here are some key issues.

Accelerating investment in emerging mobility technologies signals a transformation in the landscape within the next five to ten years. Market participants optimistic about the pace of innovation expect that by 2030, roughly half of new vehicles will be electric, nearly all new vehicles will be connected, and some (maybe one in six) will have Level 3+ autonomous-driving capabilities—such as self-driving without constant human supervision. On the same timeline, industry participants expect that approximately one-third of personal miles traveled will be attributed to micro- and shared-mobility solutions, such as bikes and ride-hailing services.

What is happening in insurance?

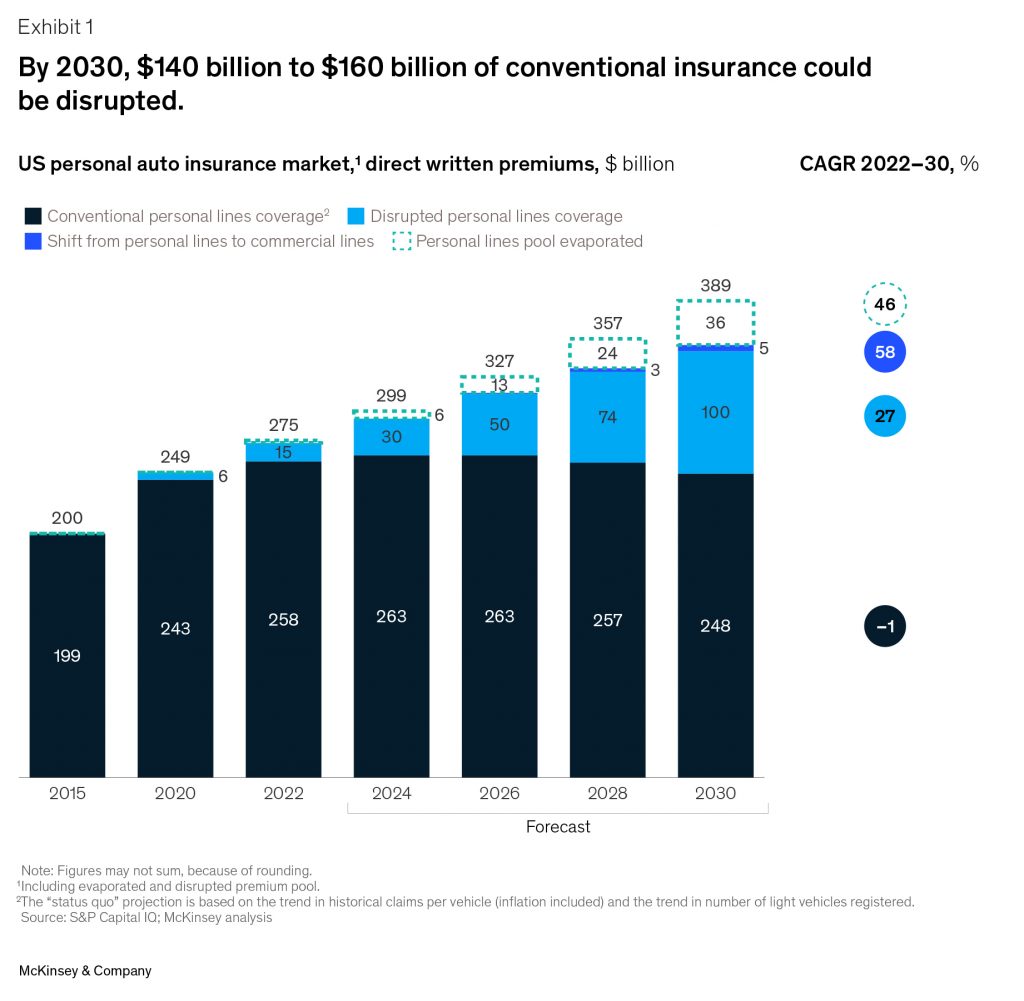

The auto insurance market is also experiencing significant change. According to McKinsey analysis, before the end of the current decade, the industry is likely to see a peak—and subsequent decline—in premiums for conventional auto personal lines coverage, currently estimated at approximately $260 billion. This scenario would see widespread, baseline adoption of advanced driver assistance systems (ADAS) features and expected consumer shifts toward greater acceptance of (and reliance on) semi-autonomous driving capabilities.

The study points out that while traditional insurance stagnates, a new auto insurance model is emerging, ripe for carriers (and, potentially, new market entrants) to capture. This $100 billion market is characterized by distinct distribution, product, pricing, and claims handling— systematically using, for example, sophisticated telematics for pricing, distribution embedded at the point of vehicle sales, and coverages for as-yet unseen generations of AVs and EVs.

Targeting this new “disrupted” auto insurance space likely requires investments in capabilities, partnerships, and know-how for market leaders. The rapid rise of EVs, for example, introduces new dynamics in risk assessment and premium calculation. The unique maintenance needs, repair costs, and battery life of EVs necessitate a recalibration of traditional insurance models. Insurers are expected to grapple with the nuances of insuring vehicles that are increasingly software driven and connected, posing distinct challenges in terms of cyber security and liability.

The authors stress that the introduction of Level 3+ AVs will further complicate the insurance landscape. As driving responsibilities shift from human to machine, questions about liability and risk assessment become increasingly complex. Insurers will need to consider the implications of software reliability, the potential for system failures, and the changing nature of driver behavior in response to autonomous technologies.

How true is the promise of driver and vehicle safety technology?

Distracted driving, largely due to smartphone use, remains the leading cause of accidents today, typically combined with pedestrian crossings or vehicles ahead braking. Data from Nauto suggests drivers face an average of six to seven distractions per hour.

Technological safety solutions hold promise in altering driver behavior and automating driving activities, potentially reducing accidents that currently result in 25,000 road deaths annually in the United States. The integration of AI and machine learning into vehicle systems offers a promising avenue, potentially transforming road safety. However, the road map to capture such benefits through automation, as of now, remains unclear for most industry players.

The researchers emphasize that regardless of the specifics facing individual companies, these technological advancements dictate an industry-wide shift in risk assessment and policy design. Insurers might need to adapt to a landscape where vehicle safety technology plays a more prominent (if not central) role in mitigating accidents.

Carriers that build a deeper understanding of the effectiveness of different safety features and their impact on driver behavior are, inevitably, the ones that are able to price and select the right risks. At the same time, the industry is called to navigate the complexities of insuring vehicles that are increasingly reliant on sophisticated software as they share roads with vehicles built before 2020 that have more-limited tech capabilities.

Will carriers insure cars or software?

The increasingly software-centric nature of vehicles necessitates a deep understanding of software reliability and cybersecurity implications. Insurers must adapt to a landscape where vehicle software plays a critical role in safety and functionality. This necessitates innovative insurance products that cater to the unique risks and liability models associated with SDVs. For example, insurers are now called to make dynamic risk assessments that consider emerging mobility contexts (such as automated driving features and OTA updates that fundamentally alter the risk profile of the vehicle) in addition to individual driver attributes (for example, age or driving record).

Furthermore, SDVs’ sophisticated software and electronic components, including sensors essential for functionalities such as autonomous driving and ADAS, in turn escalate the costs associated with physical-damage claims. For instance, a simple windshield replacement that might have previously cost about $300 can now reach $1,000 or more due to the integration of sensors and the requirement to recalibrate this equipment during replacement. Insurers face not only increased part repair costs but also around 25 to 35 percent longer repair time, according to analysis by the McKinsey Center for Future Mobility.

What role do regulators play in the auto insurance innovation race?

Rather than being seen as obstacles to technological advancement, however, regulators are committed to becoming partners to innovators today: for example, several regulator-approved driverless car pilots are operating across the United States, together with robotaxi pilots in key urban areas.

An additional—and pivotal—concern for regulators is the impact of these changes on the solvency of insurance carriers. As the growth rate in the traditional auto insurance premium pool slows or potentially shrinks because of shifts in the use of different mobility platforms and advancements in vehicle technology and safety, there is a risk that some carriers may not be able to adapt—especially if this premium pool shrinks rapidly.

At the same time, regulators are considering that, by 2030, emerging technologies will have a radical impact on claims frequency and severity. Advanced technologies, while enhancing safety, are leading to increased claims severity as a result of high costs associated with complex sensors incorporated into vehicles. This increase in severity, however, is not coupled with a drastic reduction in claims frequency. Insurance carriers unprepared for the paradigm shift in the market are under regulators’ microscope today.

Are OEMs set to disrupt insurer incumbents in the insurance landscape?

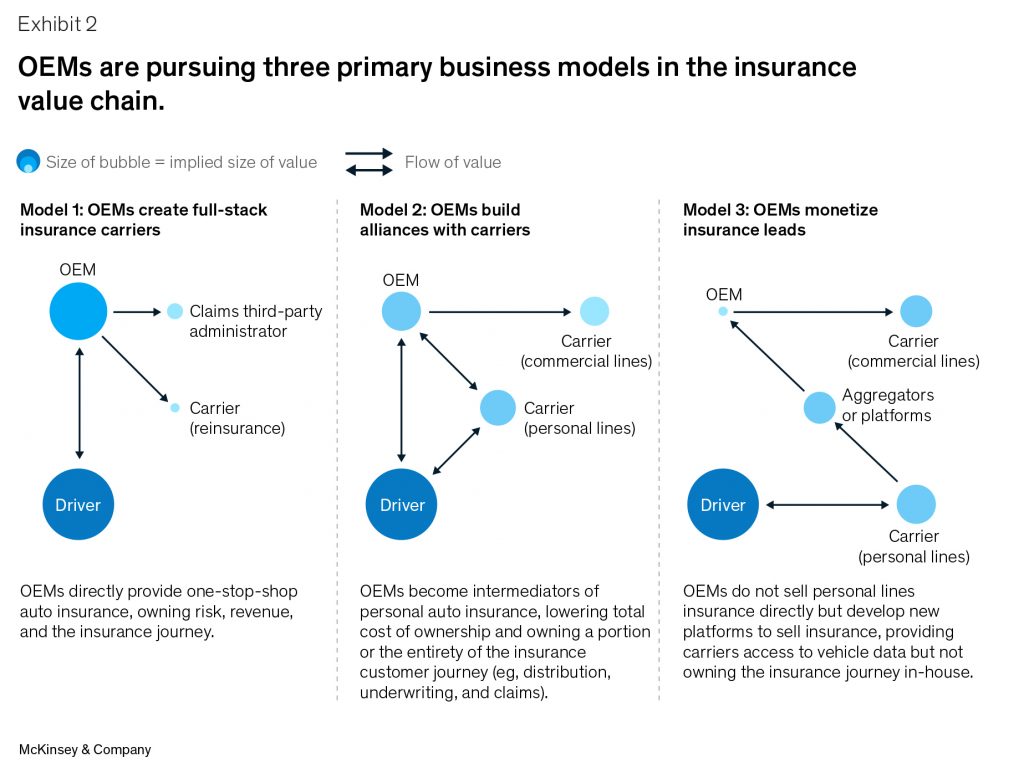

According to the study, the landscape of insurance distribution is poised for fundamental changes. Traditional strengths of carrier leaders—such as brand awareness and strong acquisition relationships—may prove to be insufficient in this new environment. As data plays an increasingly central role in risk selection, claims management, and distribution, OEMs might emerge as formidable competitors for insurers. To start, insurers may need to consider the implications of OEMs potentially treating vehicle data as a competitive asset, affecting data sharing and utilization—and opening new opportunities for collaboration with traditional insurers. Indeed, some OEMs are exploring direct insurance sales. Most of them are expected to focus on a partnership model, forming alliances with existing carriers or developing platforms to monetize insurance leads and share vehicle data.

This evolving distribution landscape, beyond challenges, presents opportunities for insurance carriers to improve margins and boost growth. At a time when premiums for conventional auto covers are declining, OEM platforms could provide a lifeline for profitability. These platforms offer a way to integrate vehicle data into policy design and underwriting, improving margins, and to access clients “at the source,” boosting growth rates.

What does the future hold for auto insurers, OEMs, and mobility players?

The auto insurance industry stands at a crossroads of technological innovation and regulatory evolution. For auto insurers, OEMs, and mobility players, these priorities are not just strategies for adaptation but are imperative for thriving in a rapidly changing landscape.

The authors indicate that auto insurers can consider the following:

- Innovate amid change. Prioritize investments in data and technology to improve risk assessment in the era of EVs and AVs.

- Forge partnerships to redefine insurance solutions. Proactively develop insurance products specifically designed for EVs, AVs, and connected vehicles in collaboration with OEMs to access critical vehicle data and expertise.

- Engage with regulators. Actively participate in regulatory discussions to shape and adapt to the changing insurance landscape.

OEMs and mobility players can employ the following:

- Collaborate for integrated insurance. Build a unique value proposition in the insurance ecosystem—especially in distribution—and enhance value for your customers.

- Maximize data value and build partnerships. Utilize vehicle data for unique services, consider beneficial data-sharing arrangements, and build partnerships across the emerging mobility landscape.

- Partner on safety initiatives. Build partnerships with auto insurers to cocreate insurance solutions with a strong emphasis on enhancing driver safety and accident prevention, integrating utilization of ADAS and other safety technologies.