Year: 2022

Shared Mobility: Where it stands, where it’s headed

Recently, the McKinsey Center for Future Mobility published a report on shared mobility. Researchers present a point of situation of the sector, reaching the conclusion that having weathered a pandemic, regulatory whiplash, and a host of other hurdles, shared mobility endures.

Here is where things stand today.

The shared-mobility market

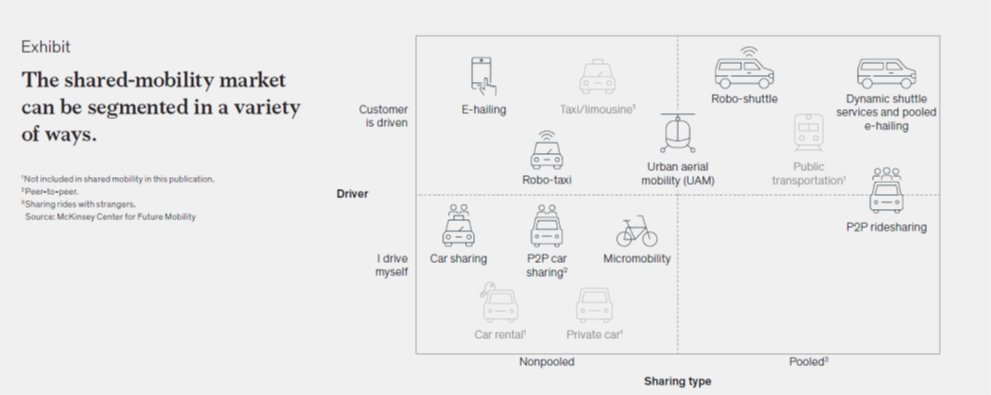

First of all, researchers, segmented the shared-mobility market along seven mobility verticals, depending on vehicle-ownership structure (private versus fleet vehicles), whether the customer is driving or being driven, and whether or not rides are shared with strangers (pooled or nonpooled). Additional layers of granularity can always be added, depending on the context (exhibit).

Market size

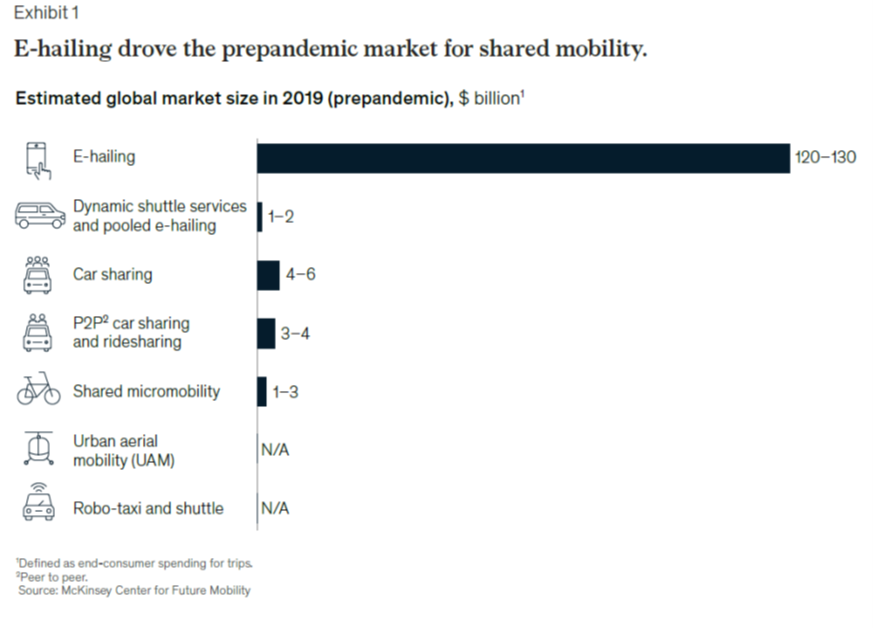

Next step is to answer to the question “how big the market is”. The shared-mobility market accounted for approximately $130 billion to $140 billion in global consumer spending in 2019 (Exhibit 1). Out of this, e-hailing accounted for the largest share, $120 billion to $130 billion, which is more than 90 percent of the total market. Taken together, car sharing and peer-to-peer car sharing account for less than 10 percent of this market, which reflects e-hailing’s higher convenience (that is, the customer is driven, can spend the time in the vehicle on other activities, and does not have to find a parking space).

Looking at the evolution of trip development over time, Exhibit 2 shows that e-hailing retained a clearly dominant role in the shared-mobility market from 2016 to 2019, showing massive growth over those four years (amount of trips tripled). Shared micromobility shows an even stronger evolution— while electric-scooter sharing did not play a major role before 2017, it accelerated in 2018 and 2019 (from fewer than 1 million trips until 2017 to greater than 160 million trips in 2019, when looking at the largest players). According to the Mc Kinsey model, micromobility could reach a consumer-spending potential of $300 billion to $500 billion globally by 2030 (combining shared and private micromobility), thus becoming three to four times larger than today’s global e-hailing market. This amount could grow even higher as the pandemic winds down and normal activities resume.

Understanding the shared-mobility market today: Investments

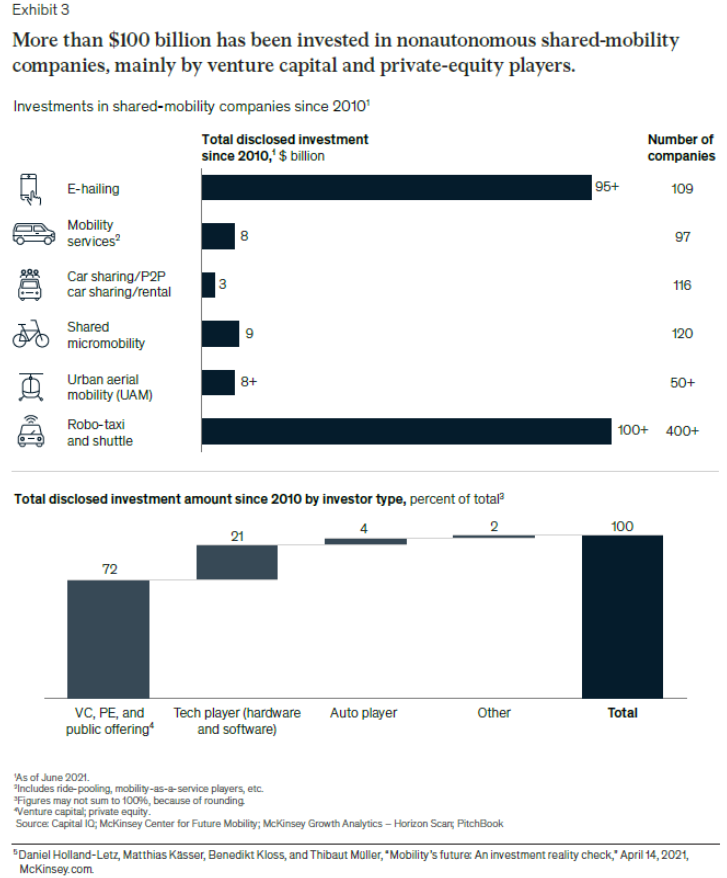

Regarding the quantity and type of investments, researchers highlighted that since 2010, more than $100 billion has been invested in shared-mobility companies (Exhibit 3). Looking deeper into types of investors, it’s not the automotive players that are investing in shared-mobility companies. Instead, around 72 percent of the total amount of disclosed investment since 2010 has come from venture capital and private-equity players, suggesting a bet on the future rather than on established and already sustainable business models.

Understanding the shared-mobility market today: Consumers

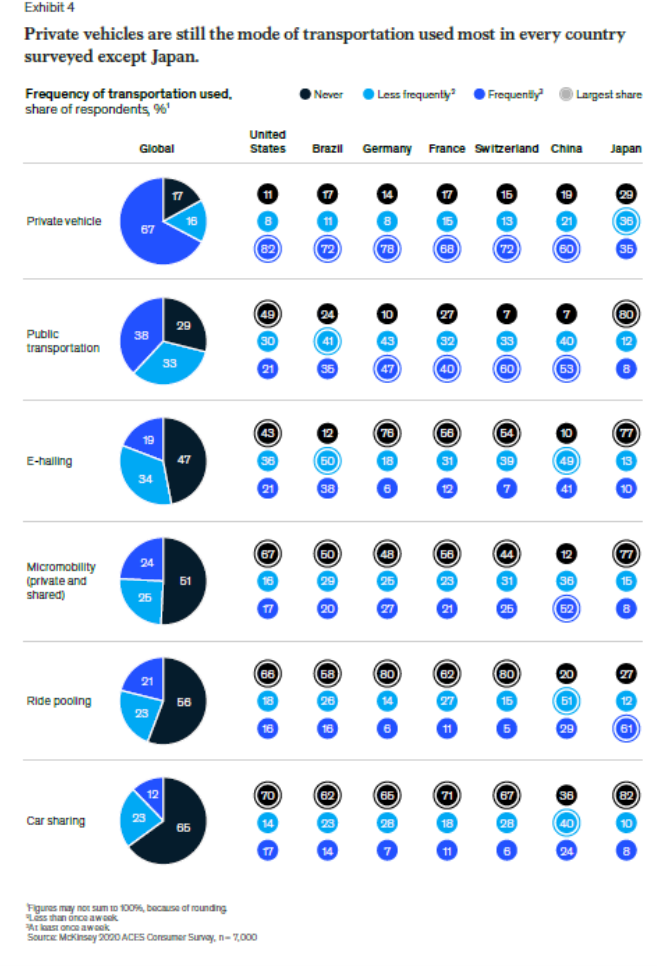

Regarding the consumers side, researchers pointed out that private vehicles remain the most popular mode of transport in almost every country (Exhibit 4). Globally, 67 percent of survey respondents said they use their private vehicles frequently (that is, at least once a week), whereas 38 percent said they used public transportation frequently. Car sharing is the least used mode on average by consumers today, which reflects the lower trip numbers. E-hailing is the most popular for consumers in Brazil, China, and the United States—in China, 90 percent of consumers stated that they use e-hailing services at least once per week.

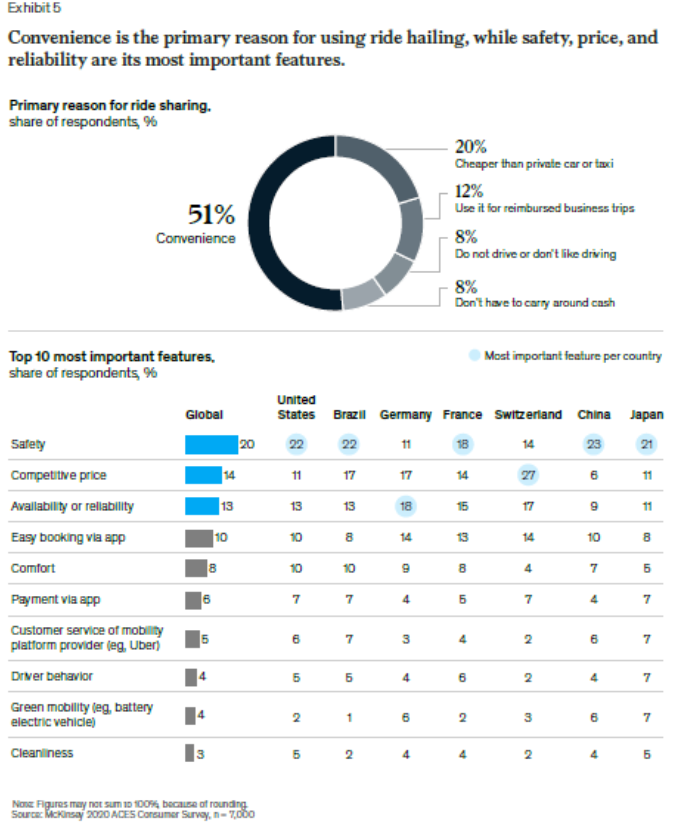

Survey respondents said that their main reason for using shared mobility is convenience (Exhibit 5). This reflects today’s dominance of e-hailing over other shared-mobility modes. The most important features of shared-mobility services for consumers are safety, a competitive price, and availability. The latter, especially, might be an important factor in shared mobility’s ability to replace private-car ownership in the long term. Notably, availability is the most important feature for German consumers.

Future mobility modes

Regarding future mobility modes, researchers concluded that when new mobility modes do arise (for example, robo-taxis or flying taxis), they expect the market potential of other modes to decrease and shift or at least remain stable through 2030. This will depend on regulatory developments (for example, cities deincentivizing or restricting private-car ownership), technology developments (for example, autonomous-driving readiness), and consumer adoption.

PS: the full report can be downloaded here:

7th Annual Motor Insurance Telematics Virtual Summit

OCTO participates in the 7th Annual Motor Insurance Telematics Virtual Summit on the 10th and 11th of February 2022.

The 7th Annual Motor Insurance Telematics Virtual Summit by Uniglobal will gather the leading motor insurance telematics experts who will talk about the current market dynamics, usage of telematics data for better pricing and customer profiling, strategies for further market penetration, usage of IoT and cloud services; exchange their experiences and views about how to increase profitability and reduce costs, as well as strengthen company’s position in the market.

On February 10th, Martin Otter – Global Insurance Stream Leader OCTO UK will be speaker at the 2:05 pm session.

Do not miss the opportunity to join us at the 7th Annual Motor Insurance Telematics Virtual Summit!

Smart mobility – an analysis of potential customers’ preference structures

Researchers Heiko Gewald (1), Thomas Shulz (1,2), Markus Bohm (2), and Helmut Krcmar (2) published an article in Electronic Markets in November 2020, named Smart mobility- an analysis of potential customers preferences structures. The article provides an a-up to date review on this issue. Here there are some of the key issues.

Big cities and towns around the world are challenged to change the mobility behaviour of their citizens and of commuters from rural areas away from predominantly private car use and toward using alternative mobility services such as public transport or bike- and car-sharing. Such a new mobility behavior paradigm would help cities address important challenges, including traffic congestion and insufficient parking, as well as air and noise pollution. Given that the percentage of the worldwide population living in urban areas is expected to increase from 50% in 2015 to 66% by 2050 (United Nations Department of Economic and Social Affairs 2015), these challenges are pressing.

One opportunity to support behavioral changes is enabled through ongoing technical progress and the proliferation of information technology (IT). The use of smartphone apps makes alternative mobility services such as car-sharing bike sharing), or ride-sharing easier and more comfortable to use. However, alternative mobility services continue to have some weaknesses which limit their contribution to the realization of a new mobility behavior paradigm.

Smart mobility app users are provided with individualized, context-aware, and dynamic recommendations for bundling mobility services for a trip from origin to the final destination. In doing so, individual customer needs and priorities, such as information about the fastest, cheapest, or most environmentally friendly bundle of mobility services are taken into account. To be effective, smart mobility apps must account for unforeseen events like short-term cancellations or delays automatically and in real-time, adapting recommended bundles dynamically. Such features would save customers time and energy by eliminating the need to search and compare myriad mobility service offerings, combine options and adapt their trip in response to unexpected changes. Ideally, customers should be able to book and pay for bundles or at least individual tickets using their smartphones.

The study stress that unfortunately, in reality, smart mobility apps do not provide this level of functionality. A number of studies show that only a few mobility providers cooperate with the providers of smart mobility apps. This has many negative effects. For example, if providers of smart mobility apps cannot access mobility provider data, their apps can only recommend a small share of all possible bundles of mobility services. In addition, the lack of provision of real-time position data limits dynamic adaptation. Furthermore, mobility providers often do not allow providers of smart mobility apps to charge customers for tickets on a ‘one-click’ basis. To date, it is unclear how the shortcomings of smart mobility apps affect their value to customers. Only a few studies have analyzed the preference structure of potential customers.

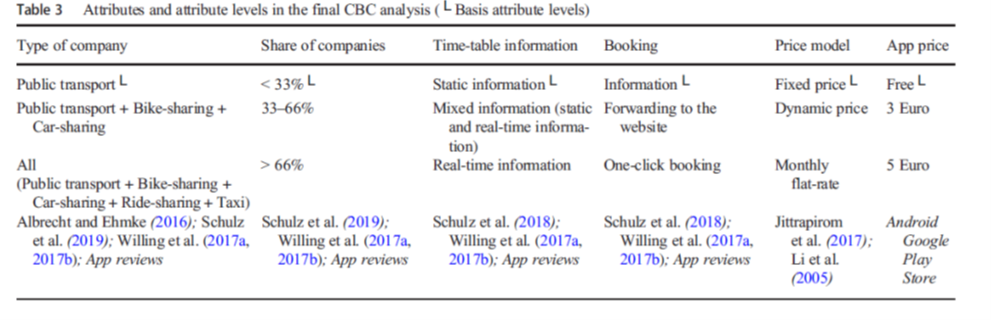

The authors highlight that the CBC analysis is a suitable and established methodology for analyzing the preferences of potential customer groups for smart mobility apps. The research focuses on analyzing potential customers’ preferences for smart mobility apps. Data collection started in July and lasted until December 2018. The data collection focused only on Germany.

Data analysis

Regardless of the participant selection, the app price was included as an attribute, as it plays a unique role in the CBC analysis. Many of the mobility apps in focus are free of charge since they are offered by mobility providers, such as public transport companies, to make their transport service more attractive. In contrast, several smart mobility apps, such as ‘Ally’ and ‘fromAtoB’, are offered by companies which do not themselves provide a transport service. For this reason, they must generate revenue via the smart mobility app (e.g., offering a fee-based app, selling advertising, charging a commission from mobility providers).

Understanding customer preference structures can help make smart mobility apps more attractive for potential customers and, hence, contribute to the reduction of private car use.

Emerging trends in the mobility sector show that “customers [are] increasingly mov[ing] away from a goods dominant perspective (e.g. buying a car)” and considering instead “the value (e.g., the flexibility and ease-of-use) offered by [, e.g.,] car-sharing applications that provide a similar mode of transportation”

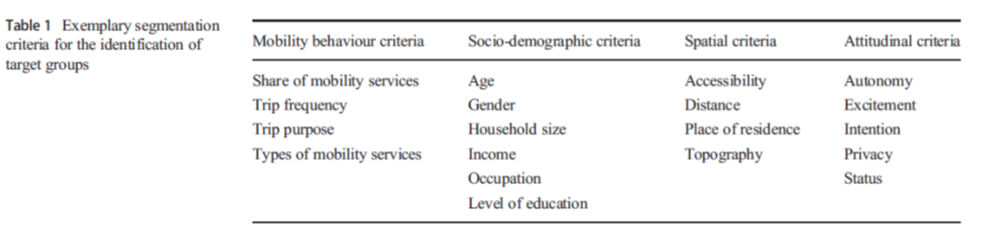

Segmenting the market into different “groups of [potential] customers with distinctly similar needs, service requirements and behavior” can provide valuable insights into how smart mobility apps should be designed.

The mobility behavior of the population can be characterized by the types of mobility services that are used over a certain period of time. The researchers conclude that since the overall goal of this study is to provide smart mobility apps that in particular contribute to switch from private car use to the use of alternative mobility services, this is the core segmentation criterion. Previous literature highlights that the route choice, and thus the linked choice of mobility services, depends individually on a high number of factors, including cost, travel time, and transfer characteristics. In the case of public transport, most of the routes require transfers “which are negatively perceived because they involve waiting time, walking, uncertainty, and loss of control over the trip”.

Similar barriers can be expected in terms of necessary transfers between all possible mobility services. Studies shows that the choice of public transport routes that include transfers can be promoted if, for example, the waiting time, reliability of connection, or information is improved. On the other hand, individual mobility behavior depends on routine and experience with mobility services, such as public transport. In turn, it is to be expected that the target groups created by mobility behavior will have different preference structures for a smart mobility app.

Discussion

Not surprisingly, young people, in particular those who live in urban areas, are early adopters of shared mobility services. (Urban) millennials also more frequently adopt apps, for example, to obtain information about the mobility services to use for a trip, or for real-time navigation. In addition, this age group considers private car ownership less important than other age groups, and they are less emotionally attached to cars. The importance of private car ownership and the emotional attachment to the car in particular among 18–24-year-olds is declining.

In contrast, especially older generations have problems accepting new IT, such as a smart mobility app.

For participants under 25 years old who use at least two mobility services per month, the ‘app price’ has a very high relative importance (41.70%) in comparison with participants who are at least 25 years old (19.76%). Interestingly, this result is not reflected in the relative importance for the attribute ‘price model’ (2.36% compared to 11.24%). When looking at the further results for those two groups, it is particularly noticeable that the younger participants have significantly lower estimated part-worths for the attribute levels ‘real-time information and ‘one-click booking’. One possible explanation is that digital natives tend to find it easy to use various apps simultaneously to find an alternative mobility service in case of a delay or in order to purchase tickets from individual mobility providers.

Earlier studies suggest that the place of residence has an effect on the preference structures of potential customers. The results of our CBC analysis reveal, in particular, that participants using at least two mobility services and who live in a town. attribute the greatest relative importance to the attribute ‘type of company’ (16.50%).

With regard to ‘mixed information’ and ‘real-time information of the attribute ‘time-table information’ no significant differences could be identified between participants who use at least two mobility services and live in big cities or towns. However, the group of participants who currently predominantly use a private car and live in a rural area attributed significantly higher estimated part-worths to these attribute levels. This could be explained by the fact that these participants have to wait a long time due to low timetable density and lack of alternative mobility services if, for example, they miss their bus due to a train delay.

The study point out that while CBC analysis is the best method to mimic the real choice decision of potential customers, it does not allow conclusions to be drawn about the use of the smart mobility app after the purchase. Future research should therefore examine continued use patterns across different groups of buyers.

While the focus of the present study is on determining the preference structure for different groups of potential customers, future work may use CBC analysis to determine their willingness to pay for smart mobility apps.

Conclusion

The researchers underline that their results indicate, among other things, that the app price is often the most important attribute affecting whether individuals choose one smart mobility app over another. In the group of participants who predominantly use a private car, however, the app price does not play a significant role, regardless of age and place of residence. Future studies should examine whether dynamic pricing can be used to increase the use of mobility services and the revenues they generate.

- Center for Research on Service Sciences (CROSS), Neu-Ulm, Germany,

- Chair for information Systems, Technical University of Munich, Germany

OCTO Connected Vehicles

Working, Living, Travelling. Everything revolves around vehicles. And when the vehicle is connected, everything becomes easier.

Stolen Vehicle Tracking

Whole protection of your car.

Monitoring the location of a truck, car or any moving vehicle using the GPS system. Extensively deployed to keep track of truck fleets, vehicle tracking ensures that the vehicles are being used properly and that they can be recovered in the event they are stolen.

Simply put, a stolen vehicle recovery system – also known as a vehicle tracking system or “GPS device” – is a telematics system that allows owners to get their stolen vehicles back.

Thanks to the alleged accuracy of the available stolen vehicle recovery systems on the market, auto insurance companies will typically provide their customers with a percent discount on their insurance policies.

OCTO Stolen Vehicle Tracking (SVT) is an end-to-end solution that, in case of theft, allows a Security Control Room (SCR) to track the vehicle and, in compliance with local law, liaise with Police to recover the vehicle.

Activation of the service can be launched:

- On demand: via a direct call by the owner to the Security Control Room

- Automatically: through an alarm triggered by a properly configured device installed in the car (e.g., car battery disconnection, car movement with ignition off, anchor alert).

The OCTO Stolen Vehicle Tracking platform gathers all the information necessary to manage the recovery from the in-car device, from the vehicle owner, and from the SCR operator. Once collected, this comprehensive and robust information is structured logically in a “theft dossier” and exported to the vehicle owner.

This Platform manages the theft dossier handover between different Countries and SCRs and tracks the vehicle, getting all the relevant data to ensure real-time localization and recovery event detection and commands.

Benefits:

- Complete solution tailorable to specific needs.

- Ensures the compliance with data protection regulations and promotes the continuous alignment with local law enforcement.

- Open infrastructure that allows the company to integrate all the participants of its ecosystem (network of SCRs distributed in different Countries, etc.) in a single IT Platform.

- Easy to modify in case of SCR supplier changes.

Optional an additional on-board device, OCTO Guardian, can be added which triggers immediate tracking upon removal or tampering of primary device

Confermata la partnership tra OCTO Telematics e Di.Di.Diversamente Disabili per il 2022 (ITA)

Roma, 24 gennaio 2022

Anche per il 2022 le attività sociali, formative e sportive promosse dalla Onlus Di.Di.Diversamente Disabili saranno supportate da OCTO Telematics, il principale fornitore di servizi telematici di analisi dati per il settore assicurativo e soluzioni tecnologiche per il Fleet Telematics e la Smart Mobility.

UN PO’ DI NUMERI

Una collaborazione che in questi anni ha permesso di ottenere risultati importanti:

• 200 i piloti che in questi anni hanno corso nel campionato italiano di motociclismo paralimpico OCTO Cup e in quello internazionale – quest’ultimo riconosciuto da FIM Europe;

• circa 10.000 gli studenti incontrati in presenza e online per il progetto di educazione stradale e sociale “Non buttate via la vita in un secondo”;

• 370 ragazzi con disabilità riportati in moto e quasi 100 le Patenti A Speciali fatte rilasciare grazie a corsi di guida specifici;

• molte le giornate di mototerapia organizzate per regalare un sorriso a chi ha una disabilità e alle loro famiglie.

“Prevenzione, inclusione e sport sono per noi valori essenziali per una società sana” afferma Emiliano Malagoli, presidente e fondatore della Onlus Di.Di. “Tutte le nostre attività vanno in questa direzione e sarebbe veramente difficile perseguirle senza il supporto di aziende come OCTO Telematics che non solo ci affianca ma partecipa in prima persona agli eventi che organizziamo. Non c’è soddisfazione più grande che condividere con loro questi bellissimi risultati e non posso che ringraziarli a nome di tutti noi, con la promessa che anche il 2022 porterà nuovi traguardi.”

Nicola Veratelli, OCTO Group CEO: “Siamo estremamente soddisfatti di dare continuità alla partnership con Di.Di. e di consolidare di anno in anno la condivisione di valori ed obiettivi comuni tra le nostre realtà. OCTO è orgogliosa di contribuire con passione ed impegno a sostenere lo sport, l’educazione e soprattutto a rinforzare la determinazione dei ragazzi che fanno parte dell’associazione.”

E’ proprio il caso di dire:

“DA SOLI SI VA PIÙ VELOCI, INSIEME SI VA PIÙ LONTANO”

Per ulteriori informazioni:

Ufficio Stampa OCTO Telematics

Adriana Zambon

+39 339.3995640