Behavioural Policy Design

This set of solutions is aimed at supporting insurance companies in expanding their customer portfolio and identifying the most suitable ones to acquire. OCTO technology does not only allow policyholders to be profiled based on risk exposure but also to incentivise risk reduction itself through the introduction of policies with premiums based on driving behavior.

Driving Habits

Thanks to this solution, insurance companies can move from a traditional approach based on static information to a dynamic model oriented to the end user, based on dynamic and aggregated data. This brings greater flexibility in the construction of fairer rates, as they are calculated on the actual use of the car.

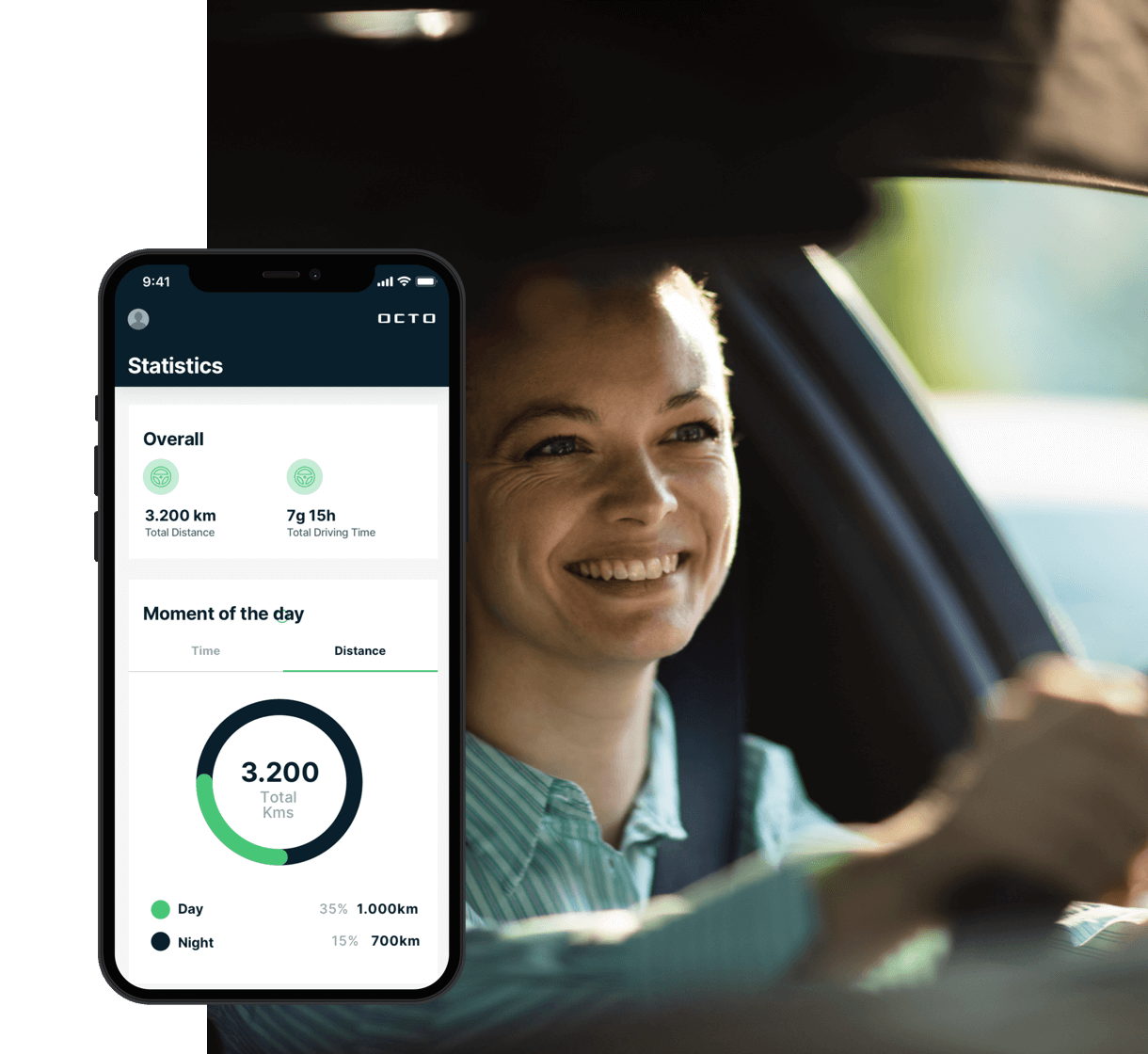

The data processed by OCTO can be easily viewed via the web, already aggregated into useful statistics for the insured and the insurer such as the type of road (urban / extra-urban / motorway), the moment of the trip (day / night or the day of the week), the duration (how log the trip and stops were) and the speed average.

Driving Behaviour

Driving style is the basis for UBI programs development. Provides insurers with a comprehensive picture of their policyholders’ driving style and helps them improve risk predictions, use a valuable tool for developing pricing models and implement targeted actions to increase profitability (incentives, coaching programs).

Driving style is defined by events such as:

Sudden braking and acceleration

Curves

Speed indicators

Duration, direction, force of acceleration triggered

Pay Per Use

Calculating the premium based on the actually travelled distance: this is the logic behind Pay-Per-Use policies. The goal is a personalised offer that rewards drivers who travel shorter distances promoting more prudent driving, fewer accidents and lower fuel consumption

The OCTO solution can be implemented taking into account several variables related to the trip like Geographical area in terms of areas of the city or region, Duration in terms of time spent driving and time windows, average speed.

Premium calculation can be made based on an annual distance estimation. When the policy expires, the deviation is calculated based on OCTO data with charge, in the case the mileage exceeds estimates, or accreditation, in case the mileage is less than the estimated.

Pay as you drive

Pay-as-You drive means a dynamic insurance premium calculation by combining a set of parameters identified by the company. The integration of telematics with IoT connectivity means that companies can automatically and accurately collect and measure driving data, therefore calculating a more accurate premium that takes into account the actual exposure to risk.

Among the most used parameters:

Kilometers / miles traveled

Counting of events at risk

Risk related to the roads traveled (based on historical data)

Duration

Speed

Request a Demo

Tell us a bit about yourself, and we’ll tell you a lot more about our solutions.