Researchers Andreas Cornet and Andreas Tschiesner, senior partners in McKinsey’s Munich office, Patrick Schaufuss partner and Ruth Heuss, senior partner in the Berlin office, published their investigation, regarding Europe’s automotive industry. The article provides an up-to-date review of this subject. Here are some key issues.

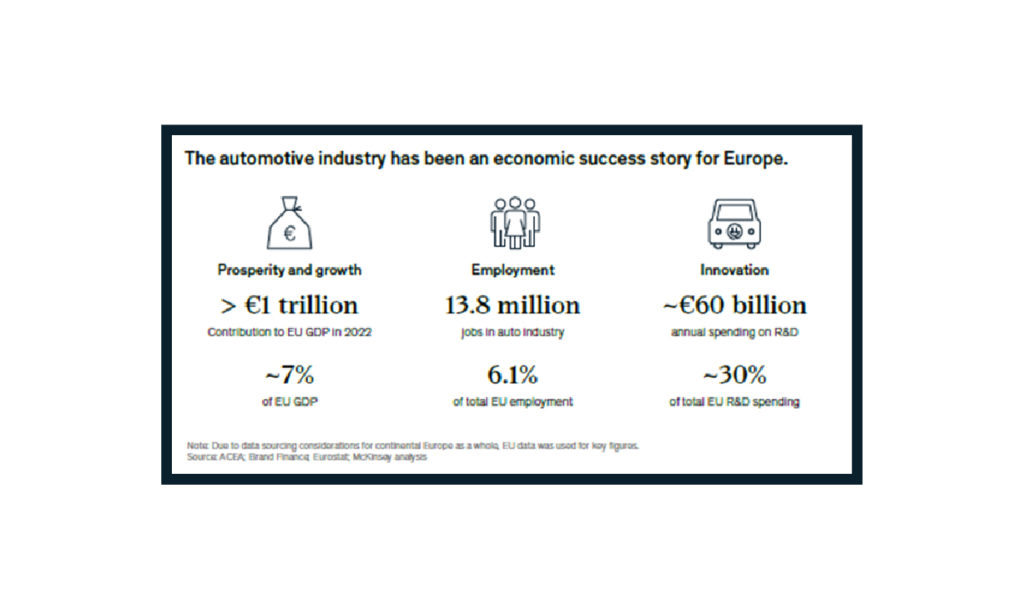

The automotive industry is a jewel of the European economy. For decades, the industry has been an important contributor to Europe’s economic growth, innovation, and prosperity, accounting for almost 7 percent of the region’s and being directly or indirectly responsible for employing almost 14 million people.

However, the status quo is being challenged and the industry faces massive ongoing transformations, such as the shift from internal combustion engines to electrified powertrains and a shift in focus from hardware to differentiation through software.

The study stress that the transition from internal combustion-engine (ICE) to zero-emissions vehicles is accelerating, with global EV sales growing 80 percent per year since 2020. The EV transition drives the industry’s emphasis away from hardware toward software and digital. According to the study, EV consumers are more than twice as likely to switch brands for better in-vehicle technology, such as advanced driver assistance systems (ADAS) features and connectivity services.

Road map for the European automotive industry

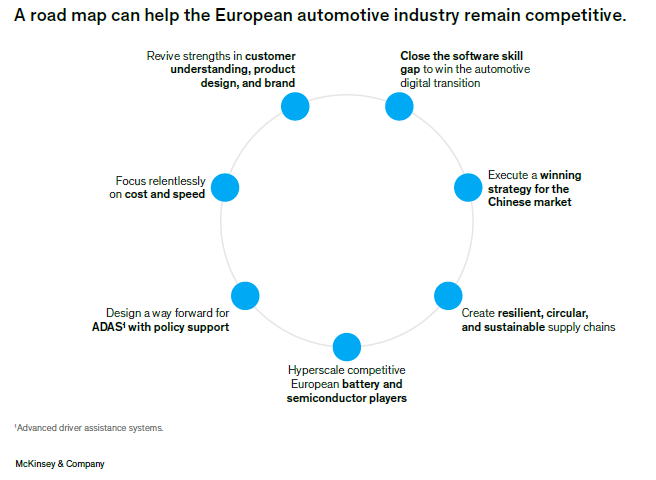

The European auto industry is in the midst of the greatest change in its history. In service of helping the industry remain globally competitive, we outline a road map of seven pillars for stakeholders to act. The time to act is now: according to the research, European automotive OEMs and suppliers earn about three times the revenue of their Chinese counterparts and five times the EBIT, which means the European industry can act from a position of strength.

1- Revive strengths in customer understanding, product design, and brand: The European automotive industry will need to extend its legacy of cutting-edge product design and superior brand value and transfer it into the new context of software-defined EVs. Traditional consumer segmentation would need to be adapted for the era of software-defined EVs, with more-detailed consumer profiles and more-granular user profiles. Owning and analyzing consumer data will enable OEMs to offer tailored mobility solutions and seamlessly engage consumers across the life cycle.

2- Focus relentlessly on cost and speed: Particularly in EVs, Chinese OEMs can turn their cost advantage into a competitive edge: the research shows that their costs are 20 to 30 percent lower than those of European OEMs. To catch up, European OEMs could drive down costs strategically. According to the study, European OEMs could close up to 20 percentage points of the cost gap by adopting structural product design, vertically integrating battery production, scaling EV production, and improving productivity. European OEMs could identify differentiating features that consumers would be willing to pay a premium for, such as brand differentiation and superior safety performance.

3- Execute a winning strategy for the Chinese market: European incumbents have lost five percentage points of market share in China since 2019, a substantial decrease. How have they done it? Chinese OEMs offer significantly lower price points, and their products are more appealing and tailored to Chinese consumers’ needs and preferences.

To implement a “local for local” strategy—in which R&D, production, and distribution are in close proximity to where products will be bought and used—the authors indicates that European players would need to adjust their operating models for the Chinese market. This starts with developing products specifically tailored for the Chinese market. Entering local partnerships across the portfolio and supply chain will also be essential to develop a strong foothold in China and to benefit from the know-how and reputations of local partners.

4- Create resilient, circular, and sustainable supply chains: To reduce bottlenecks and dependencies, the study points out that the industry will need resilient, circular, and sustainable supply chains centered on batteries, semiconductors, and green materials. To create resilient supply, localization is vital. At least in the midterm, improving the circularity of supply chains will further decrease Europe’s dependence on raw materials and components from other regions while increasing sustainability.

5- Hyperscale competitive European battery and semiconductor players: The researchers specify that a path to creating an ecosystem of technology champions consists of three elements. First, Europe should consider developing a pan-European regulatory rule book to scale high-growth firms, aligning tax standards, regulations, labor rules, and bureaucratic processes. Second, to stay at the forefront of technology, the region would need to build specialized knowledge and product innovation capabilities. Suppliers could tap into niche specialties, such as more-sustainable battery refining. Finally, the European industry would need a battery and semiconductor network, similar to the one that serves the aerospace industry. European incumbents could form strategic partnerships with emerging entrants and research institutions.

6- Design a way forward for ADAS with policy support: Advanced driver assistance systems features are increasingly important. They are becoming a key differentiator for vehicle buyers. To remain competitive, the investigation conclude that the European industry may need to form a cross-industry alliance. Players could collaborate in two main areas. The first area is where differentiation is negligible and where there are opportunities for savings. This would include standardizing sensor communication protocols, which would simplify the integration of new sensors.

The second area of collaboration is where scale and large databases could enable a faster, more robust development process for efforts including the continuous updates of software layers in maps— updates such as creating high-definition map- and location-based services.

7-Close the software skill gap to win the automotive digital transition: Software is essential to the future of the automotive industry. But according to the study, only 15 to 20 percent of current R&D workers at European incumbents have software skills, compared with almost 45 percent at new entrants. To shrink the gap, industry stakeholders would need to find holistic solutions. For example, European incumbents could create shared—or at least interoperable—software platforms across OEMs in Europe (and possibly other regions where the industry has strong partnerships) to complement individual participants’ capabilities and to avoid costly solo efforts. Early hiring, reskilling, and foreign talent can also help close the gap.

Creating an environment that enables accelerated progress

European automotive players are moving in the right direction but should consider scaling and accelerating their efforts. A clear road map such as the one the authors outline is needed to help accelerate the European automotive industry’s progress. Its seven pillars would need to be converted into actionable measures and quantifiable targets for industry stakeholders— suppliers, OEMs, players from adjacent industries, and regulatory bodies. Associations could take on a coordinating role.

The authors understand that catalysts play a significant role in implementing the road map. One is a competitive regulatory environment. Clearly defining and communicating common standards and codifying interoperability across all elements of the road map is likely to be critical.

Another critical catalyst of the European industry’s transition is EV infrastructure: the industry will need a cumulative €300 billion worth of infrastructure investments in electricity generation, the electricity grid, EV chargers, and hydrogen refueling systems through 2030.

Finally, the industry would need platforms for collaboration. As industry boundaries are redefined, three kinds of partnership will become more important: horizontal partnerships between entities in the same parts of the value chain (such as multiple car companies) for efforts such as software development or to gain a solid footing in the Chinese market; vertical partnerships between entities in different parts of the value chain (such as car companies with tech companies) to secure access to technology and talent; and cross-industry partnerships, such as collaborations between automotive players and utilities to facilitate structural goals such as seamless sector coupling.

This road map shows a way forward for a globally competitive European auto industry. The work will require action from an expansive array of regional stakeholders and a supportive administrative environment. Time is of the essence.