Researchers Max Großmann, Benjamin Köck, Janik Leyendecker, Ursula Weigl, and Romain Zilahi, representing views from McKinsey’s Automotive & Assembly Practice, published an article in 2023 regarding European mobility finance. The article provides an up- to-date review on this issue. Here are some of the key issues.

Mobility is changing. Consumers increasingly seek more-flexible mobility ownership options. At the same time, micro mobility and electrification are on the rise. The investigation points out that for mobility finance—the area of financial services that provides solutions (such as loans and leases) to support access to mobility—these changes create new opportunities to evolve and grow. The question is where revenue will move and how stakeholders should think about strategically engaging, particularly if they’re stepping outside their core businesses.

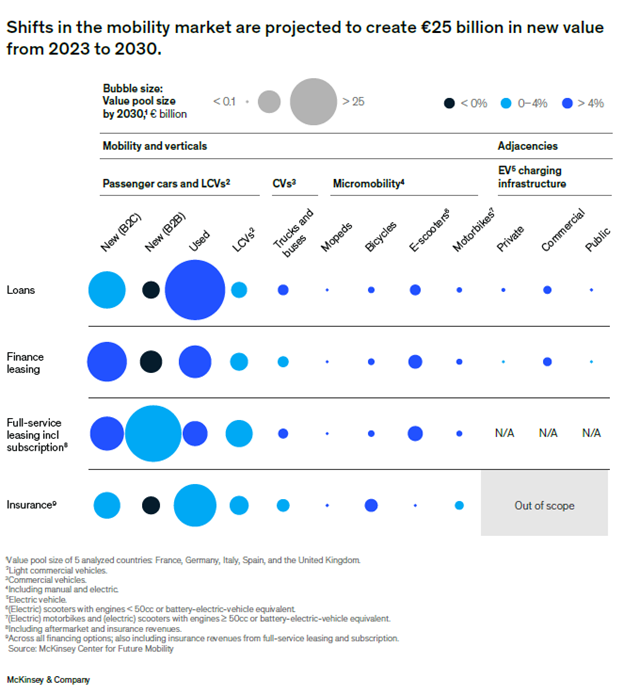

This study is based in five major European countries (France, Germany, Italy, Spain, and the United Kingdom) that together represent 50 to 60 percent of the total European market. The authors estimate that those trends will create about €25 billion of new annual revenue for mobility-finance providers by 2030 in the countries they analyzed, which represents a 4 percent compound annual growth rate for the market.

But the analysis suggests that growth potential will differ by market segment. While growth expectations are positive overall—more than 10 percent per year in some segments—the market for financial services and products for new B2B passenger vehicles is projected to decline by 1 to 2 percent per year.

Micro mobility, driven by strong growth across all market segments, will likely contribute about 5 percent of total revenue in 2030, compared with about 1 percent in 2023. EV charging infrastructure, the newest market segment for mobility-finance providers, will remain a relatively niche segment, contributing about 1 percent of total 2030 revenue. But beyond 2030, continued momentum could make EV charging infrastructure a key revenue driver.

The analysis of financial-services offerings suggests that finance leasing could increase as a share of total mobility-finance revenue from 16 percent in 2023 to 20 percent by 2030. But financing is projected to grow steadily, at less than 5 percent per year, primarily because the growing preference of consumers and companies for more flexible ownership options creates above-average growth for full-service leasing (leasing that includes other services, such as insurance or subscriptions).

Insurance is projected to grow steadily at about 1 percent per year. Diving deeper into specific segments, the investigation indicates that growth in key segments such as new B2C financing will likely stabilize after reaching high levels in recent years (which is also linked to the growing preference for pre-flexible ownership options). The researchers expect demand for used-car financing and leasing to grow rapidly: the used-car leasing market alone (including finance and full-service leasing) will have a CAGR of about 15 percent from 2023 to 2030, growing from about €3.0 billion in 2023 to €8.7 billion in 2030.

There are niche segments such as motorbike-related segments, with a potential revenue of nearly €1 billion per year by 2030. This may make these market niches a good fit for specialized financial-services providers. Many incumbents have reacted to these developments by examining opportunities to operate more efficiently and to grow inorganically, through M&A. But financial-services providers in the mobility ecosystem should also consider other strategies—and other value pools—to grow further.

Different value pools, different strategic approaches

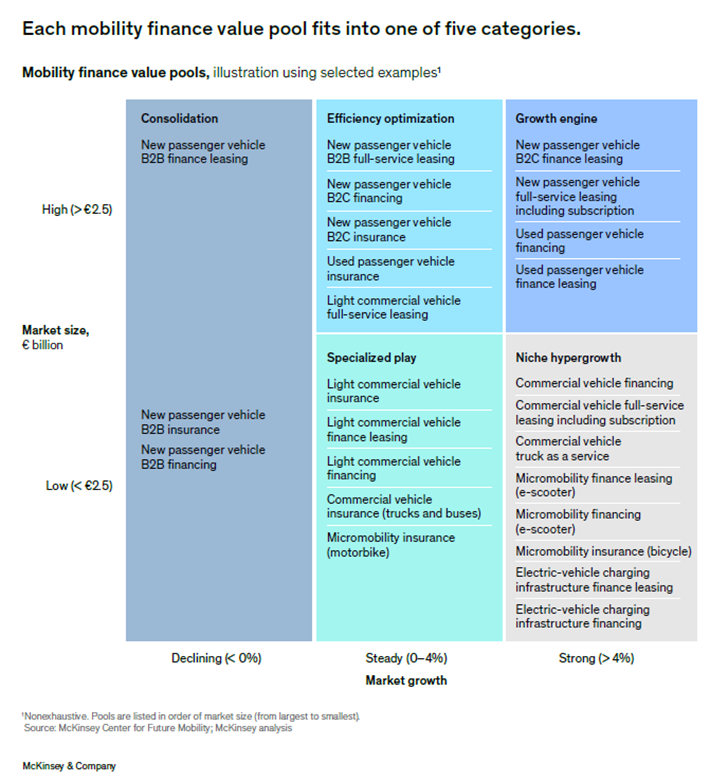

The study has structured the mobility-finance value pools into five categories, each of which requires a distinct strategic approach for successful growth.

1- Efficiency optimization

Providers of mobility financing in mature markets with limited growth potential should focus on optimizing the efficiency of their operations and managing costs. The most relevant areas are insurance for both passenger cars and commercial vehicles, commercial full-service leasing, and traditional financing for new B2C passenger cars. Providers would need to provide affordable, convenient product offerings that are easy for customers to understand and for providers to administer.

They will also need to use advanced technologies such as the cloud and AI to meet these For instance, cloud and generative AI tools can help manage risk more accurately by making it easier to gather insights from large data sets on areas such as the likelihood of defaults. effectively.

2- Growth engine

According to the analysis, some parts of the mobility financial-services market are significantly outgrowing the overall market, achieving growth rates of 5 to 18 percent. Full-service leasing, new-car subscriptions, and financing for used cars are all promising businesses with the potential to become core mobility-finance segments by 2030.

3- Niche hypergrowth

The niche hypergrowth strategy involves seizing market opportunities to develop and market innovative products. Consider how solutions around micro mobility and charging infrastructure have been rapidly scaling in response to customer demand.

The study projects that those categories will experience hypergrowth, with annual growth rates of more than 50 percent in some segments. However, the total revenue potential of these market segments is still small enough to make them niche markets—until 2030, at least.

For instance, a number of start-ups have gone to market with truck-as-a-service offerings. These comprehensive packages often include trucks, associated services, charging infrastructure, energy at a fixed rate, and enhanced offerings such as connectivity, obtained through partnerships with established companies.

Because these markets and the underlying technologies are still developing, customers’ needs are also likely still unsettled. Financial services providers will therefore have to be agile in formulating and adapting their value propositions. A test-and-learn approach can help institutions enter these markets, starting with a focused pilot—a limited initial investment—that can be scaled if it proves successful or canceled if it does not.

4- Specialized play

Characterized by small to medium-size markets with steady growth, the areas of specialized play would most likely be existing niche markets such as motorbikes and financing and leasing for light commercial vehicles. Compared with the other strategies we identify, the quality of financial institutions’ offerings—such as a broad product portfolio centered around customer needs that allows for a high level of customization—is more important here. Pursuing this strategy requires a focus on the chosen markets.

One way to enter the market is to launch a fast moving, responsive digital attacker to gain market share quickly. The focus on the product portfolio in these markets may mean limited synergies with adjacent markets, which also limits the potential to expand.

5- Consolidation

Consolidation—inorganic growth through M&A—is best suited to mature markets whose growth is declining as revenue shifts to new pockets of the market. These kinds of markets tend to involve traditional financial-services offerings for new passenger cars for B2B customers. Prime examples include finance leasing (in which a finance company legally owns an asset for the duration of the lease) and financing and insurance for new commercial passenger cars.

Because these markets are mature and growth opportunities are thin, the commercial focus would be on keeping market share steady while institutions reap the cost and efficiency benefits of consolidation.

Getting started: Identify and tap into opportunities.

The authors stress that tapping into emerging growth opportunities in mobility finance involves five critical steps:

Assess opportunities to identify which categories to enter. At this stage, decision makers should focus on evaluating their organizations’ strategic strengths and the potential for top-line synergies such as cross-selling.

Evaluate existing capabilities to identify which capabilities can help a company enter new parts of the market and whether the company should double down on those capabilities.

Enter the market with a clear immediate go-to market approach and medium-term strategy. This step should focus on efficient sales channels that can help offerings quickly gain traction among target customers.

Monitor the opportunity with predefined KPIs to adjust the approach as needed and to maximize the odds of success.

The researchers conclude that the evolving mobility market offers new opportunities for financial-services providers to evolve and grow. A combination of strategies can help these companies win a share of €25 billion of revenue. The key is to move quickly.