Car insurance serves as a cornerstone of financial security for drivers around the world, yet the specifics of coverage can vary significantly from one region to another. In this journalistic exploration, we delve into the intricacies of car insurance in Japan, comparing and contrasting it with the European model.

Understanding Car Insurance in Japan:

In Japan, car insurance, known as “Jibaisekihoken” or “Jibaihoken,” is mandatory for all vehicle owners. The minimum required coverage is “Jibaiseki,” which provides compensation for bodily injuries or property damage caused to third parties. Additionally, drivers can opt for “Jidosha Kaska Hoken” (vehicle insurance) to cover damages to their own vehicle, including collisions, theft, and natural disasters.

Like Europe, Japanese car insurance premiums are influenced by factors such as the driver’s age, driving experience, and the type of vehicle insured. Additionally, insurers may offer discounts for safe driving records and for installing approved safety devices in the vehicle.

there are 20 insurance grades. But there are 34 different types. This is the same for all automobile insurance policies in Japan.

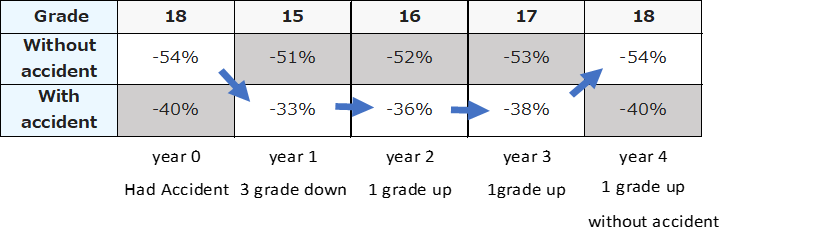

When you first purchase auto insurance, you start with the 6th grade, and if you renew your policy the following year after one year of no accidents, you will be upgraded to the 7th grade. In other words, you will be upgraded by one grade per year.

Conversely, an accident will, in principle, result in a downgrade of three grades. Exceptions are typhoons, floods, mischief, and other accidents that cannot be avoided even if the driver is careful, in which case he or she will be downgraded by one grade.

| Grade | 20 | 19 | 18 | 17 | 16 | 15 | 14 | 13 | 12 | 11 | 10 | 9 | 8 | 7 | 6 | 5 | 4 | 3 | 2 | 1 |

| Without accident | -63% | -55% | -54% | -53% | -52% | -51% | -50% | -49% | -48% | -47% | -45% | -43% | -40% | -30% | -19% | -13% | -2% | +12% | +28% | +64% |

| With accident | -44% | -42% | -40% | -38% | -36% | -33% | -31% | -29% | -27% | -25% | -23% | -22% | -21% | -20% |

This means that at 6th grade, when you first purchase auto insurance, you can sign up for a 19% discount from the Standard Price. At the highest grade of 20, you can sign up for a 63% discount from the standard price.

What is “with accident” and “without accident”?

The discount rate for premiums “with” and “without” accidents is different even for the same rating. In addition to the grade, there is an accident coefficient application period. If the accident coefficient application period is 0 years, the discount rate for accident-free policies is used; if the accident coefficient application period is 1 year or longer, the discount rate for accident-free policies is used.

The accident-free coefficient application period was introduced to correct the tendency for policyholders with accidents to be at higher risk than those without accidents, even if they were in the same grade of the previous year’s policy. The coefficient is subtracted by one year for each additional year. The maximum period for which the accident coefficient is applied is six years and the minimum is zero years.

Key Differences with Europe:

One notable difference between car insurance in Japan and Europe lies in the coverage options available. While Japanese drivers can choose from various levels of coverage, including optional add-ons for enhanced protection, European countries often have more standardized insurance packages with fewer customization options.

Moreover, the claims process in Japan may differ from that in Europe. Japanese insurers prioritize efficiency and customer service, aiming to settle claims quickly and fairly. This approach contrasts with some European countries, where bureaucratic procedures and regulatory requirements can prolong the claims process.

Cultural and Legal Influences:

Cultural and legal factors also shape the landscape of car insurance in Japan and Europe. In Japan, the emphasis on social harmony and collective responsibility influences insurance practices, leading to a focus on comprehensive coverage and prompt claim settlements.

In contrast, European insurance systems may reflect the diversity of legal frameworks and cultural norms across different countries. For example, some European countries adopt a no-fault insurance system, where each party’s insurer covers their respective damages regardless of fault, while others follow a fault-based system.

Looking Ahead:

As technology and social trends continue to evolve, the future of auto insurance in both Japan and Europe is likely to undergo further transformations. Technologies such as telematics, which monitors driving behaviour via GPS and other sensors, have the potential to revolutionize the way premiums are calculated and claims processed in both regions.

In conclusion, while car insurance serves a common purpose of protecting drivers and their assets, the nuances of coverage, regulations, and cultural influences set Japan and Europe apart. By understanding these differences, drivers can make informed decisions when selecting insurance policies and navigating the roads with confidence.