Researchers Mireia Gilibert and Imma Ribas from the Universitat Politecnica de Catalunya, Spain, published an article on Journal of Industrial Engineering and Management, September 2019, regarding the synergies between app-based car-related shared mobility services. The article provides an up-to-date review on this issue. Here are some of the key issues.

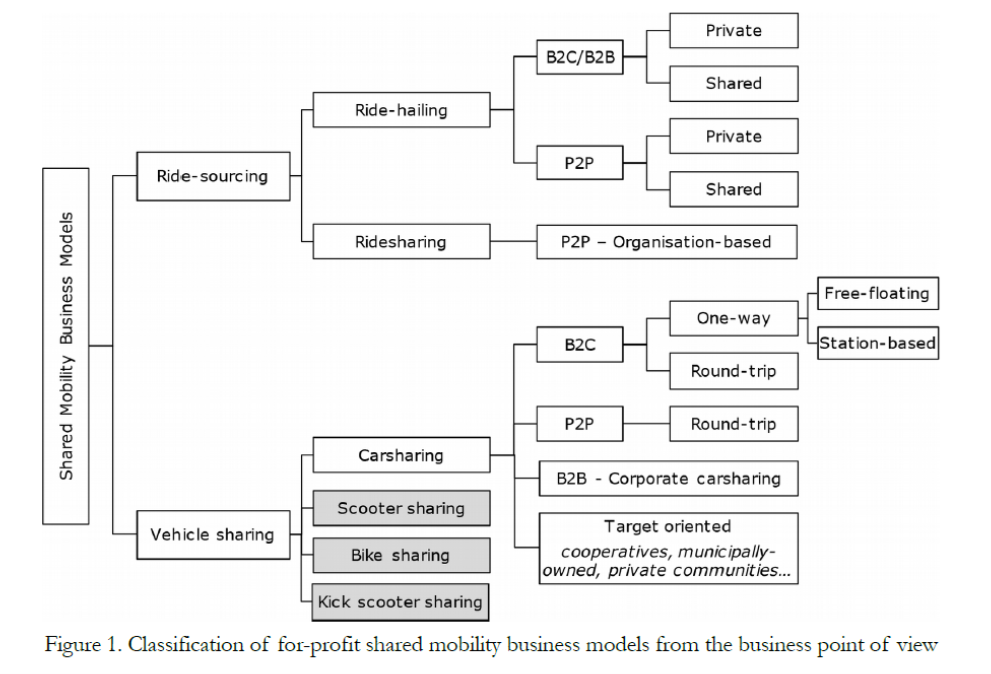

The mobility sector has seen a growth in app-based on-demand shared transport initiatives, such as renting a car by the hour or minute (carsharing) and taking a ride in a shared vehicle (ride-sourcing). These new mobility business models have changed the urban mobility sector from a limited transportation offer to a scenario full of new players offering mobility-on-demand in different ways.

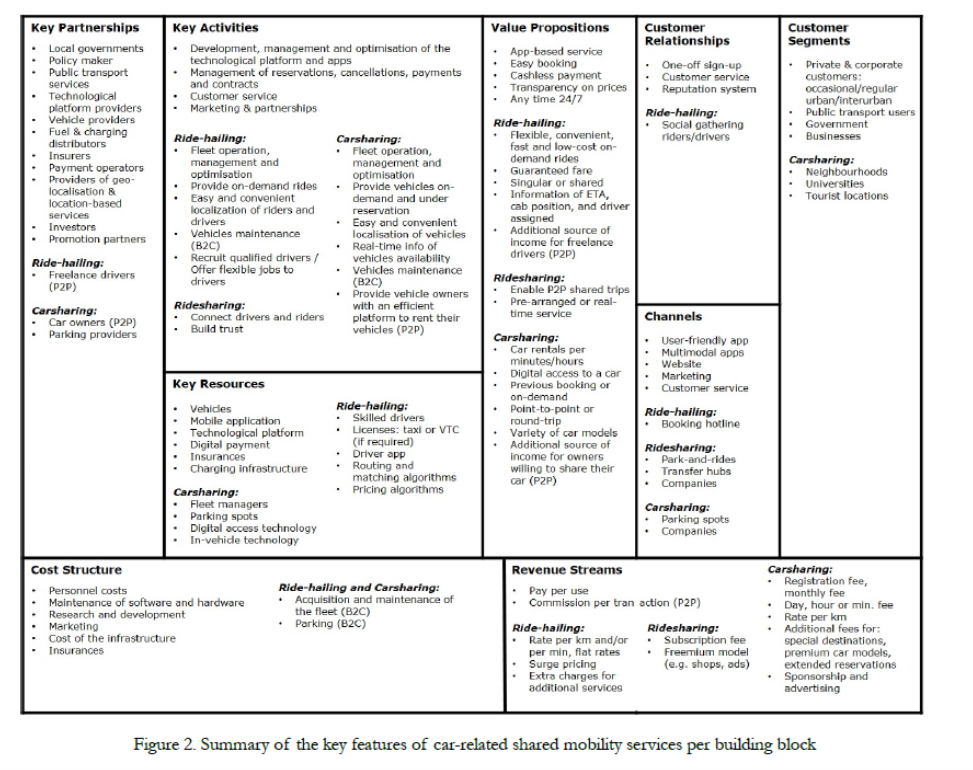

Value Propositions

The authors highlight that although each mobility service has its particular value proposition, they all have two main features in common: they are app-based and they can contribute to improve mobility, mainly in urban areas, by reducing car ownership.

Ride-hailing services are growing as an alternative to taxis, as they offer flexible and low-cost on-demand rides easily while providing a better user experience. , ride-hailing services help solve the first- and last-mile problems

On the other hand, carsharing offers easy access (no paperwork required and vehicles are usually nearby) to car rentals by the minute or by the hour, usually with digital access (via a subscription card or the app). It is available at any time of the day, on-demand or with a previous booking, and without the need to return the vehicle to the pick-up location (one-way type).

Channels

App-based mobility services mainly reach their customers through their own services’ applications, or through multimodal applications provided by Mobility as a Service (MaaS) platforms that include them. Another common and key channel for all these services is their website since customers usually look up information here about the services and even sign up as users

Revenue Streams

Emerging mobility services generally charge their customers per use; Ride-hailing services only use the pay-per-use method, charging for each ride, but allowing for different combinations.

Regarding carsharing services, their revenue model is based on a price structure that is either determined by the duration of the rental or a combination of the duration and the distance traveled. It also relies on continuous revenues and transaction-based revenues.

Key Activities

All the services explored require a technological platform as a key resource. All of them must optimise and manage their online platforms, as well as promote them in order to continue acquiring customers and establishing new partnerships. It´s also very important to keep optimized their fleet management and infrastructure for carsharing services, understanding fleet management activities to not only ensure that cars are in the proper condition (clean and charged/tank filled), but also the planning of the fleet size, relocation strategies, pricing and parking policies. These activities must also be conducted in ride-hailing services.

Key Partnerships

Local governments should be involved as stakeholders in defining the operation of shared mobility services in the cities since these strategic relationships are both key to providers willing to improve and expand their services, and to cities, willing to benefit from them to solve urban mobility issues.

Cost Structure

All three categories of the explored mobility services have similar costs, all of them being fixed costs: expenses related to the workforce, software and hardware, research and development activities, infrastructure, vehicles and the associated insurance (if owned by the service) and marketing. Additionally, B2C carsharing and ride-hailing expenses entail parking, and maintenance of the fleet as a variable cost, specifically in regard to fuelling or charging, cleaning and repairs.

Discussion

The study stresses that there are more similarities than differences among the analysed services, that they are complementary rather than interchangeable since they all cover different needs.

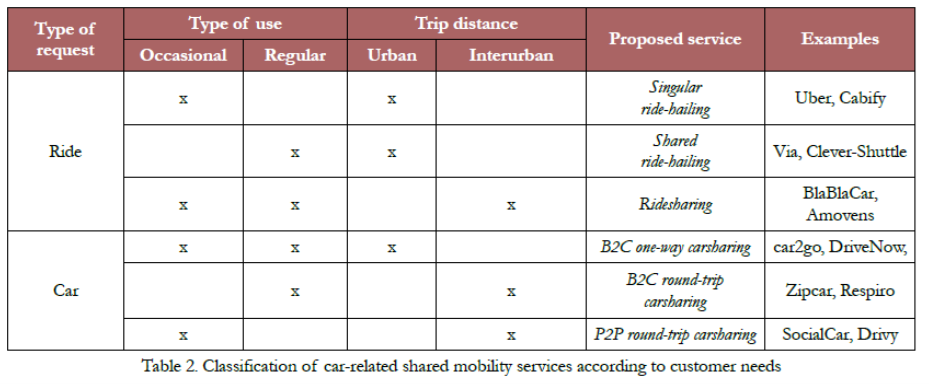

The researchers have identified that car-related shared mobility services can be classified depending on the type of request (a ride or a car), the type of use (occasional or regular), and the trip distance (urban or interurban).

For urban uses, the most suitable services are ride-hailing or one-way carsharing (which allows users to return the vehicles near their destinations at specific points (station-based) or directly on the streets (free-floating or flexible)), since both types offer on-demand and easy access to a ride or a car. Considering their revenue streams, they are suitable for a first and last-mile trip, but not for interurban travel. Instead, the round-trip model is a more suitable choice for interurban travels. Moreover, the P2P model might cover better occasional requests, whereas the B2C roundtrip model is better for regular users since their operators usually offer subscription plans. On the other hand, for commuting or long-distance trips, either occasional or regular, the most used service is ridesharing, since it is the most cost-effective option for the users.

The study also points out that the targeted Customer Segments are complementary since each type of service offers a different Value Proposition to cover the different user needs. This way, commuters may use a shared ride-hailing or a ridesharing service to commute, but also a singular ride-hailing service for leisure trips and a carsharing service for a day trip.

Therefore, if services could be provided in a combined and integrated way, the value created for the targeted Customer Segments would be higher, being the most appreciated the possibility of accessing any service through the same access point: one registration, one app, one customer service. Furthermore, the analysis of the Value Proposition proves that ride-hailing, ridesharing and carsharing have similar characteristics in that they are app-based and offer easy booking and access to the service (convenience), as well as cashless payment (convenience), and firm price quotes (price). The authors conclude tha the majority of the characteristics in the Channels and Customer Relationships blocks are common to the three studied types of services: all need a user-friendly app, a website, and marketing actions to deliver the Value Proposition.

This way, providers offering more than one service together could cut costs optimising these actions, since they could be merged. Regarding the Revenue Streams, these services are accessible through pay per use, but other revenue models could be also applied. For instance, shared mobility services could be sponsored; they could generate business with the data; or new car-related services could be offered, such as parcel delivery. Common Key Resources are vehicles and mobile applications, the technological platform, digital payment and insurances. However, ride-hailing also requires skilled and licensed drivers, as well as routing and matching algorithms, while carsharing requires parking spots, in addition to, desirably, digital access and in-vehicle technology. Common Key Activities are the development and optimisation of the platform and the corresponding apps and algorithms, as well as the management of reservations, cancellations, payments and contracts.

Concerning Key Partnerships, according to the research, the only differences are that P2P ride-hailing creates partners with freelance drivers, P2P carsharing creates partners with car owners and B2C carsharing creates partners with parking providers. Common Key Partnerships are: local governments and public transit, ICT platform providers and operators, payment operators, investors and promotion partners, and providers of vehicles, fuel or energy, insurances, and geo-localisation and location-based services.

Finally, the researchers understand that the Cost Structure is also very similar, having in common personnel costs, software and hardware maintenance, research and development activities, infrastructure and marketing; while they differ in that they have acquisition and maintenance costs of their fleet (B2C ride-hailing and B2C carsharing), and parking costs (B2C carsharing). Therefore, the Cost Structure, as well as the Key Partnerships, Key Resources and Key Activities could be also optimised if companies provide these services in an aggregated form.

In the market, there are some operators offering two mobility services from the same application: Uber and Lyft combine the offers of singular and shared ride-hailing; Amovens provides a combined offer of ridesharing and P2P carsharing; and Cabify of ride-hailing and B2C carsharing, this last option enabled through a partnership with the car rental Bipi. These services share the app, the technological platform, Channels, Customer Relationships and Key Partnerships, but they could be further optimised if they would also share the Customer Segments, the vehicles, and the fleet management. To make progress on the basis of providing an integrated service, the authors only found ReachNow in the United States, which offered, until July 2019, carsharing and ride-hailing using the same vehicle fleet: users could rent the cars through the carsharing offer and use them to organise ride-hailing trips as drivers.

From a business point of view, the main advantages for a mobility provider in offering several services in an integrated way would be: 1) higher utilisation of the vehicles, since it targets different uses. This integration would enable providers to size and optimise the fleet dedicated to one or another service depending on the predicted demand. For instance, carsharing might have higher use on weekends or on public holidays, but ridesharing and shared ride-hailing during peak hours any day of the week, and singular or shared ride-hailing at nights or to go back and forth from big events; 2) optimisation of the technological platform and related development activities, as well as fleet management and marketing activities; 3) the increase of customer loyalty, since they would no longer need more than one app to access different services.

On the other hand, relevant drawbacks that would prevent operators offering their services in an aggregated way would be: 1) the rise of the service management complexity, due to the real-time dimensioning and relocation of the fleet activities, and the provision of chauffeurs when required; 2) the increase of the cost structure if drivers are hired for providing ride-hailing services, although this cost would disappear with autonomous vehicles; and 3) regulatory issues, which differ between countries and even between regions and cities in the same country, and which could complicate the proposition and implementation of the service.

Another solution to help improves the profitability of mobility providers would be to outsource some key activities to third parties, who could offer the same service to other providers, reducing the cost of these activities. Alternatively, agreements between providers could be established to enable activities to be shared among their services. In this sense, the most relevant activities to outsource, or to be provided or shared with other providers, would be the customer service, and those related to technology (development, management and optimisation of the platform and applications) and operations (maintenance and fuelling/charging of vehicles).

Conclusions

This research has found enough similarities to suggest that aggregated offer providers could not only share some key and costly resources and activities, but also the Channels, Customer Relationships and Key Partnerships.

The authors emphasize that the business models identified, based on better use of resources, align with the forthcoming future of transportation, since autonomous cars are predicted to make carsharing services identical to private ride-hailing, which is also expected to happen with the services of shared ride-hailing and ridesharing.