The authors, Andreas Gissler, Andreas Quentin, André Gerhardy, Jan-Hendrik Bomke conducted a study called “Shared mobility: from ownership to on-demand” published in the paper “The Transforming Mobility Landscape” realized by Accenture in January 2020. In this study the authors explain how the consumption of mobility will change dramatically over the next 25 to 30 years and that the entire industries will be compelled to rethink their business models.

DRIVERS OF CHANGE

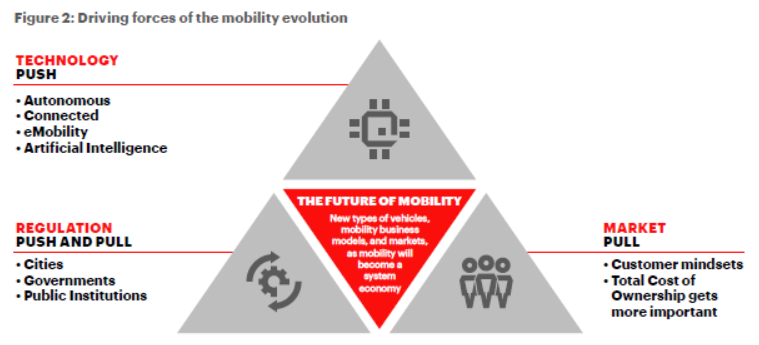

From how consumers expect to get around, to their perceptions of vehicles, to vehicle technology and design—everything about mobility will be dramatically different. The convergence of three key factors will be the driving force behind this change (Figure 2).

MARKET PULL

Consumers’ mindsets and behavior regarding cars are already substantially different from a decade ago and will continue to evolve over time, forcing companies to innovate to meet changing demands. In China, for example, more than 80 % of the population think that owning a car will be much less important and car sharing much more convenient. Similarly, consumers in Western countries believe that in the future, cars will no longer be seen as status symbols, and consumers will be more willing to use car sharing or even share their own car. Yet the full change to “as-a-service” business models will take time—it’s going to be an evolution rather than a revolution.

TECHNOLOGY PUSH

The proliferation of technological advancements is transforming the vehicle itself—from connected to electric to, ultimately, autonomous. The connected revolution is nearly complete: by 2025, all new vehicles will be connected vehicles, and 40 % of them will have embedded telematics, putting software at the center of the driver’s experience. By 2030, 30 % of all new vehicles will be electric. The true game changer comes by 2045, when half of newly sold cars will be partially or fully autonomous — which will have a massive impact on current consumption patterns by turning drivers into riders. As vehicles and their accompanying technologies evolve, they will continue to disrupt mobility-related industries, making possible entirely new business models and spurring even greater inventions.

REGULATION PUSH AND PULL

By 2050, about two-thirds of the global population will live in cities, more than double the figure in 1970.

Without government action, this will mean more cars and trucks on the streets, forcing commuters to spend more time in traffic jams and generating more pollution that threatens both people’s health and the environment. Regulators need to rethink how they address traffic to fulfill their mission to make worry- free and clean, sustainable mobility available to a city’s inhabitants. We’re already seeing cities taking steps to that end, such as new regulations to meet sustainability targets, additional tolls or fees for personal vehicles, and restrictions on goods delivery by trucks in the city center. As such actions become more widespread, they will create greater incentive for people and businesses to find ways other than driving their own vehicles to get around increasingly populous cities.

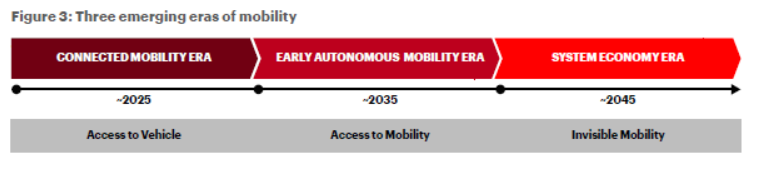

THREE ERAS OF MOBILITY

As the preceding forces evolve, we’ll see a corresponding evolution in mobility itself—embodied by three distinct eras (Figure 3).

CONNECTED MOBILITY ERA

In the first, the Connected Mobility Era, consumers still place a priority on access to vehicles themselves. However, these vehicles will grow increasingly intelligent, enabling new service models. Car sharing also will continue to expand, encouraged by government regulations to limit private cars and reduce congestion on city streets, as well as the more favorable economics of vehicle usage compared with ownership.

EARLY AUTONOMOUS MOBILITY ERA

As new autonomous vehicles become viable for the masses, we’ll enter the Early Autonomous Mobility Era, when consumers prefer access to mobility-as-a-service over access to a vehicle. Cities and public institutions, in turn, will have to respond by investing in their infrastructure and putting in place the right regulations to encourage the deployment of autonomous technology that boosts access to mobility.

SYSTEM ECONOMY ERA

When fully autonomous cars become commonplace, the System Economy Era begins to take shape. Through the emergence of various forms of mobility services, mobility moves to the background. Consumers will see mobility as a utility, available on-demand without much thought about how it happens—much like they view electricity in their homes today. In this era, cities and public institutions will have to fully regulate mobility to accommodate this “invisible” utility. Furthermore, automotive OEMs will need to adapt not only their marketing and sales strategies, but also the way vehicles are designed.

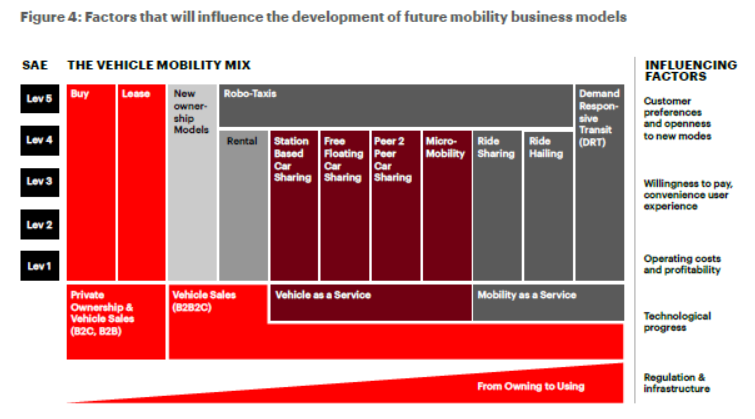

THE VEHICLE MOBILITY MIX AND INFLUENCING FACTORS

What does all this mean to the mobility ecosystem’s players and how they make money? To be sure, the mobility evolution will create massive challenges for traditional OEMs and their current business models. But it also opens up tremendous new opportunities, not to mention compelling new revenue streams for any company willing to think boldly about how and where it can play as these eras unfold.

In the future, companies will generate revenue from mobility in three primary ways:

- Vehicle Sales: the traditional automotive business of designing, building, and selling cars to consumers and companies to satisfy long-term mobility needs

- Vehicle-as-a-Service: the vehicle (such as cars, bikes, or scooters) is offered as-a-service to consumers to satisfy short- and mid-term mobility needs

- Mobility-as-a-Service: mobility itself is offered as-a- service—whereby the consumer is no longer the driver, but the rider—to satisfy short- and mid-term mobility needs

When analyzing the respective development of each business model, one must consider five main influencing factors clustered around customers, the public sector, and mobility industry players (Figure 4).

From a customer perspective, three big factors will drive the choice of mobility mode: customers’ willingness to pay for mobility; the convenience they expect from the service; and other customer preferences, such as environmental values or desire for predictability. A general openness to new ways to get around also will be critical to the success of innovative new business models.

The public sector also plays a vital role in the future success of new forms of mobility. This includes delivering the required infrastructure (be it roads or 5G networks), creating the appropriate regulatory environment, and orchestrating the mobility mix in countries and cities (the last of which is also key to defining the availability and supply of mobility modes).

Last but not least are the mobility industry players, which will need to drive the technological progress needed to make new business models possible and to determine how to make those models profitable (which means operating cost management will be key to long-term business success).

Although each factor on its own can significantly influence mobility’s future, the interplay of all factors— as well as geographical and regional differences in customers and public sector players—will ultimately decide what tomorrow’s mobility mix actually looks like. The real game-changer will be autonomous technology. When autonomous vehicles reach Level 5—full automation—driverless cars will be able to operate on any road and in any conditions a human driver could negotiate. This will make robo-taxis technologically and, at some point, economically feasible, which could spell the end for other mobility services based on Vehicle-as-a-Service (VaaS) and Mobility-as-a-Service (MaaS) (Figure 4).

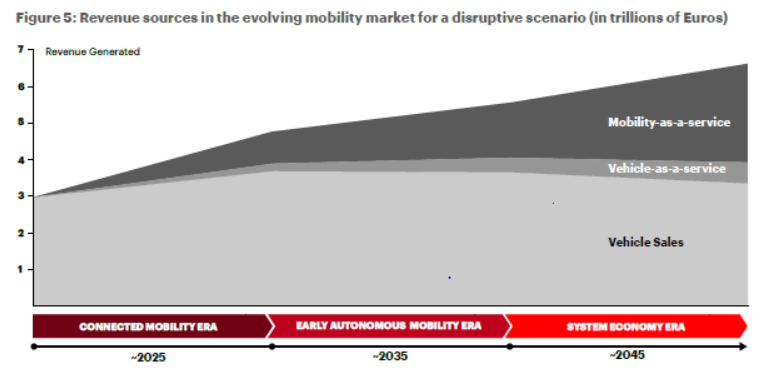

Let’s look in more detail at the three dominant types of business models we can expect to see in the coming years, how they’ll likely evolve, and their projected revenue trends over time (Figure 5).

VEHICLE SALES

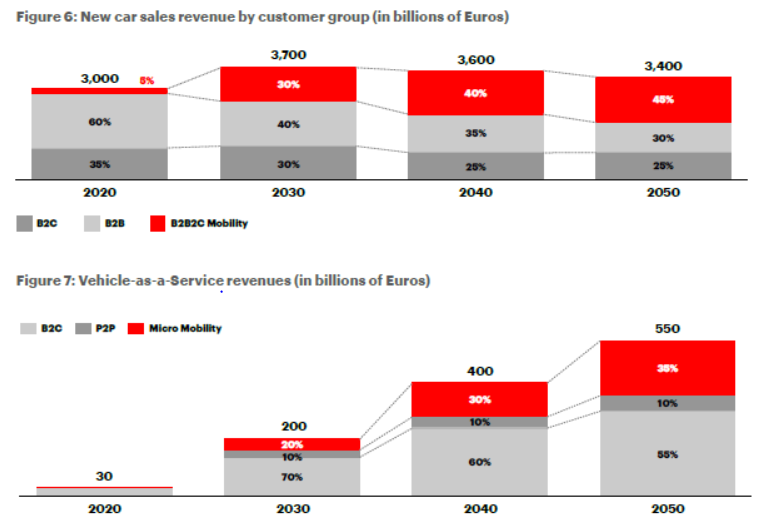

Regardless of the era, vehicles will still be needed and a business model that includes producing vehicles for sale will remain viable. In fact, vehicle sales will still account for the largest proportion of total revenue generated by mobility players across all three eras, and global new car sales will grow by 1.6 % annually until 2050, spurred by economic and global population growth. Revenues from new car sales also will increase throughout the Connected Era, peaking during the transition to the Early Autonomous Mobility Era (2030) before entering into a slow, gradual decline back in line with today’s figures.

However, the types of vehicles made, who buys them, and the revenue generated will certainly change (Figure 6). In 2050, vehicles will mainly be sold to corporate fleets and mobility fleet operators to provide short-, medium- and long-term mobility on-demand.

Privately owned vehicles will remain the primary mode of transportation in rural and suburban areas. Because they’ll be those consumers’ primary mode of transportation and will have greater comfort features and superior technology compared with vehicles used in fleets, they’ll likely command a premium price.

VEHICLE-AS-A-SERVICE (VaaS)

As connected vehicles become increasingly autonomous, VaaS will become increasingly popular. VaaS business models will emerge to provide vehicles and the necessary infrastructure to flexibly book and share vehicles that fulfill short- and medium-term mobility needs. The most prominent of these business models will be business-to-consumer (B2C) car sharing and micro-mobility (akin to today’s electric scooters), with people-to-people (P2P) car sharing playing a minor role due to people’s reluctance to let strangers drive their vehicles.

However, despite strong growth between 2020 and 2040, VaaS will only play a minor role in the new mobility environment (accounting for less than 10 % in 2050) (Figure 7). Among the factors that will impede further growth of VaaS are asset-heavy operations within B2C car sharing, lack of trust between P2P car sharing members, high turnover needs in micro- mobility, high operations and insurance costs, overall regulation, and a general difficulty in scaling. Hence, VaaS can be characterized as a transition stage toward full-fledged mobility-as-a-service (MaaS) offerings and, importantly, a big step toward getting consumers more familiar with and confident in mobility services.

MOBILITY-AS-A-SERVICE (MaaS)

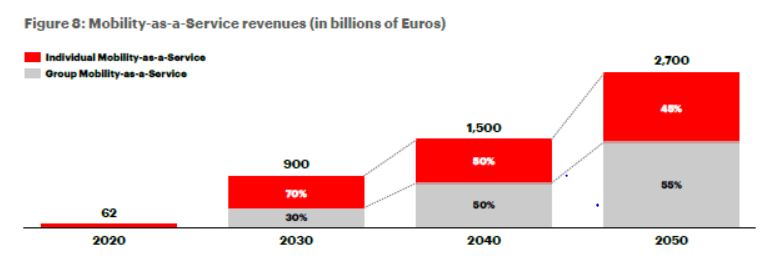

MaaS business models will disrupt and transform the way people consume mobility—becoming the option of choice for short-term mobility needs, turning drivers into riders, and effectively relegating mobility to the background by making it a passive rather than active pursuit. MaaS will come in two “options”: Individual MaaS will include initial business models such as ride hailing, which eventually will give way to the more economical “robo-taxis.” Group MaaS will be primarily focused on-demand-responsive transit, whose value proposition is effectively and efficiently organizing ride pooling and which, with effective partnering, can serve as a complement to or even replace existing public transportation networks.

As MaaS becomes more prevalent, the revenue it generates will grow accordingly—increasing more than fortyfold between 2020 and 2050 (Figure 7), when it will comprise 40 % of the mobility industry’s total revenues. The MaaS market will be characterized by a high degree of development and be highly dependent on technology advancements and regulation. For instance, fully autonomous driving will be key to driving down MaaS’s marginal costs, enabling cost and price leaders to dominate the market.

KEY TAKEAWAYS

- The future mobility ecosystem and value chain will reshuffle the deck for everyone involved, as disruptive new players enter the market and mobility service providers, cities, and other stakeholders will shift the balance of power and key strategic control points across the ecosystem. In that context alliances and strategic partnerships are necessary, to generate critical mass to scale mobility services in a very short time.

- Until now the mobility ecosystem has mostly failed to generate sustainable profits because of customers’ unwillingness to pay and high operational and financial costs. As a result, a clear “separation of duties” is necessary among vehicle manufacturers (which should run their mobility efforts apart from their traditional car-making business); suppliers (such as fleet operators); and the mobility providers themselves to build the right set of capabilities and resources to given the severe competition. Doing so will be critical to reducing marginal costs, optimizing asset utilization, building the right product offering, and generating sustainable profits.

- When it comes to scaling mobility offerings, the mobility ecosystem not only faces operational and regulatory barriers, but also highly differentiated and diverse customer demands. Customer expectations for how they actually will consume mobility differs significantly across continents, countries, and regions, which leads to significant offering and operational complexity. Therefore, the mobility ecosystem must, first and foremost, take a regional or local approach to be able to deliver the services customers want.

- While scaling businesses to minimize costs and reach a critical mass is central to all mobility providers, regulators will be called on to regulate and orchestrate mobility offerings across cities to create an environment in which mobility can grow sustainably. Determining and supporting the right mixture of mobility offerings will be key to giving residents access to new forms of mobility, managing competition, and learning how to best organize new forms of transportation.

- Last but not least, the mobility revolution is only possible if all stakeholders can build the necessary infrastructure that, for example, enables the use of connected and autonomous vehicles at scale and efficient mobility operations. This, in turn, hinges on regional orchestration and collaboration, as well as significant public investments.